Navigating Trust Accounts and Tax Liability.

Prepared by: Lucent Consultancy

In the modern Zimbabwean business landscape, particularly within the construction and legal sectors, the use of Trust accounts to hold client funds, deposits, and advance payments has become standard practice. While the legal necessity of separating client funds from operational capital is well-understood, the tax treatment of these funds, specifically when they migrate from a “Trust” environment to a “Business” environment, is a frequent flashpoint during ZIMRA audits.

At Lucent Consultancy, we have noted a growing trend of tax authorities scrutinizing these transfers. Many firms mistakenly believe that funds held in a Trust are “shielded” from tax until they are officially booked as revenue. This is a dangerous misconception.

Drawing on the Income Tax Act, the VAT Act, and the Capital Gains Tax Act [Chapter 23:01] lets unpack an exhaustive analysis of the tax treatment of these transactions.

The Anatomy of a “Trust” Transfer: Substance vs. Form

The core issue that attracts ZIMRA’s attention is the characterization of the funds. A common scenario involves:

- Receipt: A construction firm receives a 30% upfront deposit from a client for a project.

- Staging: The money is placed in a “Trust” or “Client” account to denote it is not yet “earned.”

- Migration: As project milestones are reached, the firm transfers these funds from the Trust account to the Business (Operational) account.

The Taxpayer’s View: “The money is not mine until the work is done; therefore, it is not taxable yet.”

ZIMRA’s View: “The firm has received the money. The timing of when it is ‘earned’ for accounting purposes is irrelevant to the ‘time of supply’ for VAT or the ‘date of accrual’ for Income Tax.”

The “Substance Over Form” Doctrine

Zimbabwean courts, in line with global tax jurisprudence, have consistently applied the substance over form principle. If a Trust is created solely to delay tax obligations, ZIMRA will look through the Trust structure (piercing the corporate/trust veil) and assess the tax based on the economic reality of the transaction.

Income Tax: The Accrual Doctrine

Under the Income Tax Act, income is taxable when it is “received by or accrued to” the taxpayer.

The Myth of “Waiting for Invoicing”

Many firms wait to raise an invoice before recognizing income. However, Section 8 of the Income Tax Act uses the phrase “received by or accrued to.” If you have received the cash into a Trust account that you control or have beneficial interest in, that money has arguably “accrued” to you.

The Lucent Consultancy Position:

If the Trust account is a vehicle where the business has the right to the funds, even if the work is incomplete, the funds must be treated as Gross Income. Transferring them to the Business account is merely a movement of cash, not an event that creates or delays tax liability.

Value Added Tax (VAT): The Critical “Time of Supply”

VAT is often the biggest danger zone for firms using Trust accounts. Under the VAT Act [Chapter 23:12], the “Time of Supply” is the earlier of:

- The date an invoice is issued; or

- The date any payment (or deposit) is received.

The “Trust Trap”

When a firm receives a deposit into a Trust account, they have, in the eyes of the law, received a “payment.”

- The Error: Firms often wait until they move the money from the Trust account to the Business account to issue the tax invoice and account for VAT.

- The Consequence: This is a late declaration of VAT. ZIMRA will impose penalties (up to 100% of the tax due) and interest for the period between the deposit date and the date they discover the “hidden” receipt.

Strategic Advice: Your VAT output tax must be accounted for in the tax period during which the deposit hits the Trust account, not when it is transferred to the operating account.

Capital Gains Tax (CGT): Analyzing Chapter 23:01

The Capital Gains Tax Act provides a specific framework for assets. While most Trust-to-Business transfers involve operational cash flow, complexities arise when firms use Trusts to hold property or “specified assets.”

The Definition of “Specified Asset” (Section 2)

The Act defines a “specified asset” as:

(a) Immovable property;

(b) Marketable security;

(c) Rights or titles to property (including mineral rights).

Transferring Property to a Trust

If your firm transfers a “specified asset” into a Trust for “protection,” this is a disposal.

- Deemed Disposal: Under Section 8(2)(b), where a person disposes of a specified asset otherwise than by way of sale, it is deemed to be a sale at the “fair market price.”

- The Risk: If you move property into a Trust, ZIMRA may treat it as a disposal, triggering immediate Capital Gains Tax.

- The Valuation Risk: If the transaction is between “connected persons” (the business and its own Trust), ZIMRA has the power under Section 14 to determine the fair market price. If they deem the value higher than what you reported, you will face an additional assessment.

The “Lucent” Caution on CGT

Ensure that if you are moving assets, you are utilizing the specific exemptions where applicable (e.g., Section 15: Transfers between companies under the same control, though note that trusts are not companies). Always consult a tax professional before re-structuring asset ownership.

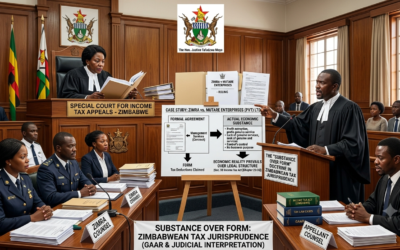

5. Case Law and The Courts

Zimbabwean courts have been firm on the independence of ZIMRA’s assessment powers.

Relevant Precedents:

- Sabeta M v Commissioner General: ZIMRA (12-HH-079): The court emphasized that ZIMRA is not permitted to refuse to assess or issue a CGT certificate once tax is paid. This protects the taxpayer but underscores the need for voluntary and accurate reporting.

- Rouse S v ZIMRA (25-HH-315): This case highlights the complexity of “accrual” in agreements. The court focused on the substance of the agreement.

The Lesson: Courts will not rescue taxpayers who use Trusts to obfuscate the reality of their transactions. The best defense against ZIMRA is a clear, transparent audit trail that distinguishes between “funds held for a client” (a true liability) and “funds held as a deposit” (pre-paid income).

6. How to Build a “Tax-Ready” Trust Structure

If you must use a Trust for operational purposes, ensure you can answer “Yes” to these questions:

- Is the Trust Deed Notarised? An un-notarised trust is merely an arrangement, not a legal entity in the eyes of ZIMRA.

- Is there a clear “Client vs. Firm” distinction? Does the Trust hold money for third parties (true trust) or is it just a secondary account for the firm’s cash? If it is the latter, ZIMRA will aggregate it with your business income.

- Is the “Time of Supply” tracked? Are you accounting for VAT on deposits immediately upon receipt in the Trust account?

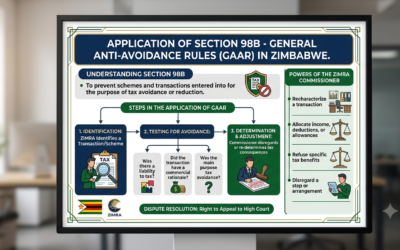

- Is the “Trust” a shell? If the Trust lacks a commercial purpose other than tax avoidance, expect ZIMRA to trigger the General Anti-Avoidance Rule (Section 98 of the Income Tax Act).

Lucent Consultancy: Your Partner in Compliance

Navigating the complexities of Zimbabwean tax law—from the Capital Gains Tax Act to the VAT Act—is not something you should face alone. At Lucent Consultancy, we help firms structure their operations to be both efficient and fully compliant, preventing “hidden” tax liabilities from becoming business-ending audits.

Our Services Include:

- Tax Health Checks: We audit your Trust-to-Business flows to ensure no “late declaration” penalties are lurking in your books.

- Audit Representation: If ZIMRA has already knocked on your door regarding Trust funds, we provide the technical expertise to manage the inquiry.

- Strategic Structuring: We advise on how to handle client deposits legally and efficiently without triggering unnecessary tax events.

Don’t wait for a ZIMRA assessment letter to realize your Trust accounting is non-compliant.

Contact Lucent Consultancy Today:

- Email: [email protected]

- Phone: +263771030251

Disclaimer: This guide provides general information based on current Zimbabwean legislation. Tax laws are subject to change, and individual circumstances vary. This document does not constitute formal legal or tax advice. Please consult with our team regarding your specific business situation.