The “Substance Over Form” Doctrine in Zimbabwean Tax Jurisprudence

Prepared by Lucent Consultancy

Tax compliance and tax planning exist in a state of perpetual, delicate tension. On one end of the spectrum is the sacred right of every taxpayer to structure their commercial affairs in a manner that minimizes their tax liability—a principle famously articulated in the English case of Inland Revenue Commissioners v Duke of Westminster [1936] AC 1. On the other end lies the state’s sovereign interest in preventing the artificial erosion of its tax base through schemes that lack commercial reality.

In Zimbabwe, this tension is mediated by the “Substance Over Form” doctrine and its statutory companion, the General Anti-Avoidance Rules (GAAR). This comprehensive treatise unpacks the “Substance Over Form” doctrine as it applies to Zimbabwean tax law, analyzes landmark court cases, translates complex legal disputes into accessible layman’s terms, and offers critical, actionable insights for both corporate taxpayers and tax administrators (ZIMRA).

The Philosophical and Legal Divide

At its core, the “Substance Over Form” doctrine dictates that tax liabilities should be determined by the actual economic reality of a transaction (its “substance”) rather than the legal label, documentation, or accounting wrappers the parties have chosen to place around it (its “form”).

This doctrine finds its roots in Roman-Dutch common law, which forms the basis of Zimbabwe’s legal system, through the Latin maxim:

Plus valet quod agitur quam quod simulate concipitur

This translates literally to: “What is actually done is of more value than what is simulated or pretended.”

The Clash of Two Fundamental Principles

In Zimbabwean tax disputes, the court is almost always asked to balance two competing doctrines:

- The Duke of Westminster Principle (Legal Form): A taxpayer is entitled to arrange their affairs so that the tax attaching under the appropriate Acts is less than it otherwise would be. If they succeed in ordering them so as to draw themselves out of the net, then, however unappreciative the tax authority may be, they cannot be compelled to pay.

- The Substance Over Form / Simulation Principle (Economic Reality): If a transaction is a “sham” or “simulation” designed to hide its true character to escape tax, the court will look through the facade, examine the real transaction, and tax it accordingly.

In the modern fiscal environment, ZIMRA has grown increasingly aggressive in challenging transactions that appear legally sound but lack commercial or economic substance.

The Statutory Framework in Zimbabwe

While the common law doctrine of simulation allows courts to look at the substance of a transaction, the Zimbabwean Parliament has codified these principles in powerful statutory provisions.

A. Section 98 of the Income Tax Act [Chapter 23:06]: The GAAR

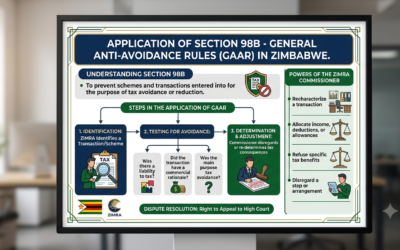

Section 98 is the primary engine of anti-avoidance in Zimbabwean direct taxation. It grants the Commissioner-General of ZIMRA the unilateral power to disregard, recharacterize, or restructure a transaction for tax purposes if they believe it constitutes a tax avoidance scheme.

For ZIMRA to successfully invoke Section 98, four distinct statutory criteria must be met:

┌────────────────────────────────────────────────────────┐

│ THE FOUR HURDLES OF SECTION 98 │

├────────────────────────────────────────────────────────┤

│ 1. An "Arrangement" │

│ A contract, scheme, plan, or transaction exists. │

├────────────────────────────────────────────────────────┤

│ 2. Tax Avoidance │

│ The scheme results in a reduction or avoidance of │

│ tax liability. │

├────────────────────────────────────────────────────────┤

│ 3. Abnormality │

│ The scheme was entered into in an abnormal manner │

│ or created abnormal rights/obligations. │

├────────────────────────────────────────────────────────┤

│ 4. Sole or Main Purpose │

│ The main purpose of the scheme was tax avoidance. │

└────────────────────────────────────────────────────────┘

If these four criteria are satisfied, ZIMRA is empowered to “determine the liability for any tax… as if the transaction, operation, or scheme had not been entered into or carried out, or in such manner as the Commissioner-General deems appropriate for preventing or diminishing such avoidance.”

B. Section 98B and the Thirty-Fifth Schedule: Transfer Pricing

Introduced to modernize Zimbabwe’s tax system, Section 98B mandates that transactions between “associated persons” (related parties or multinational group companies) must be conducted in accordance with the arm’s length principle.

This is essentially a specialized, statutory application of “substance over form.” Even if a domestic company has a contract (form) to pay its South African parent company a massive management fee, ZIMRA can look at the substance: Would an independent third party pay this amount for these services? If the answer is no, the transfer pricing rules allow ZIMRA to adjust the taxable income.

C. Section 67 of the Value Added Tax Act [Chapter 23:12]

Like the Income Tax Act, the VAT Act contains a powerful anti-avoidance provision. Under Section 67, if any transaction or scheme has been entered into solely or mainly to secure a VAT benefit in an abnormal manner, ZIMRA can disregard the scheme and assess VAT based on the true underlying commercial supply.

Understanding the Common Law Doctrine of Simulation

Before looking at specific Zimbabwean court rulings, we must understand how Roman-Dutch common law defines a “simulated transaction.”

Historically, the benchmark test was established in the landmark South African case of Zandberg v Van Zyl (1910 AD). Chief Justice Innes ruled that:

“The Court must be satisfied that there is a real intention, definitely ascertainable, which differs from the simulated intention.”

Under this traditional test, a transaction was only simulated if there was element of dishonesty or deception—a “holding out” of one agreement to the world while secretly agreeing to something else.

The Modern Shift: The NWK Test

This traditional view was dramatically expanded by the South African Supreme Court of Appeal in Commissioner for SARS v NWK Ltd (2011 (2) SA 67 (SCA)). The court ruled that simulation is not just about a hidden secret agreement. Instead, courts must ask whether the transaction makes commercial sense:

“If the transaction is structured in an extraordinarily complex manner to achieve a tax benefit, but lacks any genuine commercial purpose, the transaction is simulated, even if the parties intend to perform according to its terms.”

In Zimbabwe, our courts look to South African jurisprudence as highly persuasive. Consequently, the NWK case shifted the battleground. ZIMRA no longer has to prove that a taxpayer is “lying” about their contract; they only have to prove that the transaction lacks commercial reality and was structured solely to escape the tax net.

Landmark Court Cases Analyzed in Layman’s Terms

To truly understand how these principles operate in real-world business, we must analyze how the Zimbabwean courts have resolved disputes over substance versus form. Below are four key cases.

Case 1: Travel Agents (Pvt) Ltd v ZIMRA (15-HH-285)

The Dispute

Imagine you run a travel agency. When a traveler wants to buy an airline ticket for $1,000, you collect the full $1,000 from them, keep $100 as your commission, and send $900 to the airline.

- The Travel Agent’s View: “I am just a middleman (an agent). The $900 belongs to the airline; it was never my revenue. Therefore, I should only pay VAT on the $100 commission I earned.”

- ZIMRA’s View: “Looking at your bank accounts, you received $1,000. When you gave the client an invoice, you didn’t say ‘commission: $100, airline cost: $900’. You just billed them $1,000. You don’t have a signed agency contract with the airline. In our eyes, you are a retail merchant selling tickets. Therefore, you must pay VAT on the entire $1,000.”

The Court’s Ruling and Legal Reasoning

The High Court of Zimbabwe ruled in favor of ZIMRA. The court emphasized that while the travel agent argued that the substance of their industry is agency, the form of their actual documentation did not support this.

The court laid down a harsh reality for taxpayers:

- The Burden of Proof: Under Zimbabwean tax law, the burden of proving that an amount is not taxable rests entirely on the taxpayer.

- The Default State: If your invoicing, bank accounts, and lack of written contracts make you look like a Principal (a main seller), the court will treat you as a Principal, regardless of industry norms.

- The Invoicing Trap: If you issue a single invoice for the gross amount without clearly segregating your commission from the principal’s funds, you have chosen a “form” that attracts VAT on the entire sum.

┌────────────────────────────────────────────────────────┐

│ TRAVEL AGENTS (PVT) LTD vs. ZIMRA: │

│ THE AGENCY DOCUMENTATION CHECK │

├────────────────────────────────────────────────────────┤

│ TAXPAYER CLAIMED: COURT RULED: │

│ "We are just agents." "Your paperwork says otherwise."│

│ │

│ [x] No formal written contracts with airlines. │

│ [x] Invoiced clients for full ticket price. │

│ [x] Mixed client funds into main business accounts. │

├────────────────────────────────────────────────────────┤

│ RESULT: Taxed as a Principal on gross ticket sales. │

└────────────────────────────────────────────────────────┘

Case 2: Zimbabwe v CRS (Pvt) Ltd (High Court, HH 728-17)

The Dispute in Layman’s Terms

A Zimbabwean company (CRS) needed to use heavy machinery and logistical equipment. To acquire this equipment, they set up a complex transaction structure involving a related company in South Africa. Instead of buying the equipment directly or entering a standard lease, the parties entered into structured cross-border leasing and logistics arrangements.

- The Taxpayer’s View: “We are legally leasing these assets from our South African sister company. The lease payments we send to South Africa are fully deductible business expenses, which reduces our taxable income in Zimbabwe. Furthermore, they are exempt from certain taxes due to our specific corporate structuring.”

- ZIMRA’s View: “This is a paper-driven illusion. The South African company is a shell with no real operations. You structured this ‘lease’ abnormally to shift profits from Zimbabwe to South Africa, where tax rates or withholding mechanisms were more favorable. In substance, this is not a genuine lease; it is a profit-shifting scheme.”

The Court’s Ruling and Legal Reasoning

The High Court upheld ZIMRA’s assessment, validating the use of the Section 98 General Anti-Avoidance Rule. The court’s reasoning highlighted the concept of “abnormality”:

- The Abnormality Test: The lease terms were completely abnormal compared to how independent leasing companies operate. The rights, obligations, and pricing structure did not make commercial sense.

- Profit Shifting: The sole purpose of inserting the South African entity into the supply chain was to create a deductible expense in Zimbabwe, thereby reducing the domestic tax base.

- The Power of Recharacterization: The court confirmed that under Section 98, ZIMRA did not have to accept the “lease” label. ZIMRA was legally permitted to recharacterize the lease payments as deemed dividends or disallowed expenses, triggering severe back-taxes and penalties.

Case 3: Commercial Bank IT Software & Simulation Case (High Court, 2026)

The Dispute in Layman’s Terms

A prominent Zimbabwean commercial bank entered into an intra-group software licensing agreement. The bank paid licensing and maintenance fees to a related IT entity within the same corporate group.

- ZIMRA’s View: “This intra-group loan and licensing structure is simulated. The related IT company did not have the capability to develop this software, and the ‘loan’ terms make no commercial sense. In substance, these payments are a disguised distribution of profits (dividends) meant to avoid withholding taxes and claim unearned deductions under Section 15(2)(a).”

- The Bank’s View: “This is a legitimate commercial arrangement. While we are related companies, we actually behave as debtor and creditor. We keep detailed records, we track the loan, we obtained Exchange Control approval for the repayments, and we actually made physical payments. The software provides an enduring, functional benefit to our banking operations.”

The Court’s Ruling and Legal Reasoning

In a major victory for the taxpayer, the High Court rejected ZIMRA’s claim of simulation. The court’s reasoning provides a critical shield for legitimate businesses:

- Simulation Must Be Proved, Not Presumed: ZIMRA cannot simply look at a related-party transaction, see a tax benefit, and cry “simulation.” The tax authority must bring concrete, factual evidence proving that the parties had a “different, hidden intention.”

- The “Commercial Reality” Test: The court examined the actual conduct of the parties. It noted that the bank actually made repayments, maintained active debtor tracking, and sought regulatory (Exchange Control) approvals. This behavior is consistent with a genuine commercial transaction.

- Accounting Entries are Not Confessions: ZIMRA had argued that because of certain accounting credits and entries in the bank’s books, the bank had admitted to taxable income. The court firmly rejected this, stating that accounting treatments are merely persuasive evidence, not absolute law. Legal rights and tax realities override bookkeeping entries.

- The Capital vs. Revenue Clarification: The court did, however, find that because the licensed software provided an “enduring benefit” to the bank, the license fees were capital in nature and could not be fully deducted as an immediate operational expense. Instead, the bank had to claim statutory capital allowances over time.

Case 4: Zimbabwe v IAB Company (High Court, HH 32-22)

The Dispute in Layman’s Terms

A local Zimbabwean company (IAB) paid massive “management and technical service fees” to its foreign parent company.

- The Taxpayer’s View: “Our parent company in Europe provides us with strategic guidance, IT support, and executive management services. We have a signed Management Services Agreement (MSA) that requires us to pay them 5% of our gross turnover. This is a legitimate business expense.”

- ZIMRA’s View: “You have a beautiful written contract, but where is the proof that any ‘management’ actually took place? We want to see emails, reports, flight tickets of visiting managers, software logs, or timesheets showing exactly what work was done. Without this, the contract is a shell, and the substance of the transaction is a non-deductible profit remittance.”

The Court’s Ruling and Legal Reasoning

The High Court ruled in favor of ZIMRA, reinforcing the strict evidentiary threshold in substance-over-form disputes.

┌────────────────────────────────────────────────────────┐

│ THE "IAB COMPANY" SERVICE TEST │

├────────────────────────────────────────────────────────┤

│ DOCUMENTARY FORM: OPERATIONAL SUBSTANCE: │

│ [✓] Signed Management [x] No timesheets or logs. │

│ Service Agreement [x] No written deliverables. │

│ [✓] Corporate Invoices [x] No proof of local benefit.│

├────────────────────────────────────────────────────────┤

│ RESULT: Deduction Disallowed due to lack of proof that │

│ services were actually rendered. │

└────────────────────────────────────────────────────────┘

The court held that:

- Paper is Not Enough: A written agreement (form) is completely meaningless for tax purposes if the taxpayer cannot prove that the services described in the agreement were actually rendered in reality (substance).

- The Local Benefit Rule: The taxpayer must prove not only that a service was performed, but that it directly benefited the Zimbabwean operating entity’s income-producing activities.

- The Consequence of Failure: Because the taxpayer failed to provide contemporaneous, physical evidence of the services, ZIMRA was fully justified in disallowing the entire deduction, resulting in a massive income tax assessment plus a 100% penalty.

Strategic Takeaways for Businesses and Taxpayers

For corporate leaders, directors, and finance teams in Zimbabwe, the “Substance Over Form” doctrine represents a major operational risk. If ZIMRA successfully reframes your business transactions, it can lead to back-taxes, interest, and penalties that can bankrupt a business.

To protect your organization, apply these four strategic protocols:

Protocol 1: The Principle of “Documentary Realism”

Your contracts must match your operational reality. If you draft an agreement, your operational staff must be trained to execute it exactly as written.

- Action: Conduct annual “Stress Tests” on all major contracts (especially related-party agreements). Ask your operations team: “If ZIMRA asks for proof that we are following Section 4 of this contract, what physical evidence can we show them today?”

Protocol 2: Solve the “Agency Trap”

If your business model relies on acting as an intermediary, clearing agent, or broker, you are highly vulnerable to being taxed on gross cash flows rather than net commission.

- Action:

- Segregate Funds: Set up dedicated Trust or Escrow bank accounts for client funds. Never commingle client money with your operational capital.

- Delineate Invoices: Ensure your fiscal invoices explicitly display the principal’s cost and your service fee as separate, clear line items.

- Expose the Principal: Your contracts with clients must clearly state that you are acting as an agent and do not assume ownership or liability for the underlying goods/services.

Protocol 3: The “Commercial Purpose” Rule of Thumb

Before entering into any complex corporate restructure, intra-group loan, or asset transfer, ask yourself:

$$\text{Does this transaction make sense if the tax benefit is completely removed?}$$If the transaction is only viable because of the tax savings, it is highly likely to fail a ZIMRA GAAR audit under Section 98.

- Action: Ensure all board resolutions and strategic planning documents detail the non-tax commercial reasons for a transaction (e.g., operational efficiency, risk mitigation, regulatory compliance, asset protection).

Protocol 4: Assemble a “Contemporaneous Evidence File”

In tax law, the court will not accept retrospective explanations. You must prove your case using documents created at the time of the transaction.

- Action: For all related-party transactions (management fees, royalties, shared service centers), build a living “Substance Binder.” This binder must contain:

- Detailed timesheets of foreign consultants/managers.

- Project deliverables, reports, and slide decks.

- Direct emails and correspondence demonstrating the advisory services.

- Proof of actual payment (bank telegraphic transfers).

Strategic Takeaways for Tax Administrators (ZIMRA)

The “Substance Over Form” doctrine is a powerful sword for tax administrators, but it is not a blank check to ignore the law or harass legitimate businesses. The courts have established clear boundaries that ZIMRA must respect to maintain administrative credibility and avoid costly defeats in litigation.

Takeaway 1: Respect the Burden of Proving Simulation

ZIMRA cannot simply look at a transaction that reduces tax and label it a “sham.”

- The Legal Boundary: As affirmed in the 2026 High Court Commercial Bank case, the burden of proving that a transaction is a simulation (that the parties had a different, hidden intent) rests heavily on the Revenue Authority. ZIMRA must produce concrete, factual evidence of simulation; they cannot rely on suspicion or mere assumption.

Takeaway 2: Commercial Context and Industry Realities Matter

Tax auditors must look beyond the balance sheet and understand the regulatory and economic realities governing an industry.

- The Legal Boundary: In the Commercial Bank case, the court noted that the parties’ transaction was heavily influenced by central bank regulatory capital requirements and exchange control rules. ZIMRA must evaluate transactions within their specific regulatory and macroeconomic environments rather than in an academic vacuum.

Takeaway 3: Procedural Discipline is Non-Negotiable

The courts are increasingly critical of ZIMRA’s administrative and procedural failures.

- The Legal Boundary: When a taxpayer objects to an assessment, ZIMRA must act within the statutory timelines (e.g., determining objections within three months). Serial corrections, delayed responses, and issuing amended assessments after court proceedings have commenced undermine ZIMRA’s legal standing. A strong technical tax case can easily be lost if ZIMRA fails to maintain procedural discipline.

Takeaway 4: Distinguish Between “Form Errors” and “Shams”

There is a massive legal difference between a taxpayer who has poor documentation (e.g., Travel Agents (Pvt) Ltd) and a taxpayer who is engaging in a dishonest simulation.

- The Legal Boundary: Where a taxpayer acts in good faith but has chosen the wrong legal label or accounting treatment, ZIMRA should apply the correct tax treatment under the law (allowing capital allowances, adjusting transfer pricing) rather than automatically imposing maximum 100% fraud penalties. Penalties must strictly follow actual, proven tax evasion, not simple administrative errors.

Comparative Analysis: Summary of Key Doctrines

To help corporate boards and tax legal teams navigate these complex concepts, the table below provides a comparative summary of the legal doctrines that govern substance, form, and tax planning:

| Dimension | The Westminster Principle | The “Substance Over Form” Doctrine | General Anti-Avoidance (Section 98 GAAR) | Transfer Pricing (Section 98B) |

| Core Concept | Taxpayers may arrange their affairs to pay the minimum tax. | The true economic reality overrides the legal label. | Abnormal transactions with tax avoidance as the sole/main purpose are voided. | Related-party transactions must reflect market (arm’s length) rates. |

| Primary Target | Legitimate, efficient tax planning. | Dishonest shams, simulations, and hidden agreements. | Highly complex, artificial, or “abnormal” tax schemes. | Profit shifting, transfer mispricing, and unproven group fees. |

| Key Question Asked | Is the legal structure technically valid under the law? | Did the parties actually intend to do what their contract says? | Does this transaction make commercial sense without the tax benefit? | Would independent third parties have agreed to these same terms? |

| ZIMRA’s Burden | Must prove the law explicitly taxes the arrangement. | Must prove a mismatch between intent and outward appearance. | Must prove: Arrangement, Tax Benefit, Abnormality, and Sole/Main Purpose. | Must prove the pricing deviates from comparable market transactions. |

The Path Forward for Zimbabwean Firms

In the modern Zimbabwean tax landscape, the days of relying on a “cleverly drafted contract” to shield high-risk tax structures are officially over. ZIMRA’s audit teams are increasingly trained to look past the paper, examine bank feeds, review operational emails, and apply the “Substance Over Form” doctrine.

However, as the courts have repeatedly affirmed, this does not mean that legitimate tax planning is dead. If your business transactions are built on genuine commercial logic, backed by impeccable contemporaneous documentation, and executed with operational consistency, they will survive even the most aggressive ZIMRA audits.

The Lucent Compliance Checklist for Corporate Boards

Before approving any major transaction or related-party agreement, ensure your team can answer “Yes” to these four questions:

- The Reality Check: Do our operations staff actually perform the duties exactly as described in this contract?

- The Commerciality Check: If ZIMRA removes the tax savings from this structure, does the transaction still make business sense for our shareholders?

- The Agency Check: If we act as a middleman, are we holding client funds in a separate, un-commingled trust account?

- The Evidence Check: Do we have an active, living folder of physical deliverables (emails, logs, reports) to prove that our related-party expenses are real?

Navigating ZIMRA audits and structuring high-value transactions requires a careful blend of legal expertise and operational reality. Do not wait for a ZIMRA audit letter to find out that your contracts lack substance.

Contact Lucent Consultancy Today for Expert Tax Health Checks and Audit Representation:

- Office Address: [Insert Address Here]

- Email: [email protected]

- Phone: +263771030251

- Website: https://lucent.co.zw