Analysis the Value Added Tax Act [Chapter 23:12]

This analysis synthesizes the provided legislative text, focusing on the mechanism of “Standard Rated” supplies and the legal landscape of VAT in Zimbabwe.

The Standard Rated Mechanism

In the context of the VAT Act, “Standard Rating” is essentially the default tax position. The Act functions on a principle of exclusion: any supply of goods or services made in the course or furtherance of a trade by a registered operator is subject to tax unless specifically provided for as either Zero-Rated or Exempt.

- The Charging Provision (Section 6): Tax is levied at a rate fixed by the Charging Act (Finance Act) on the value of supplies made by a registered operator.

- Defining the Taxable Supply: To be standard rated, the transaction must meet the definition of a “supply” and be made in the course of a “trade” (as defined in Section 2).

- The “Trade” Hurdle: Judicial precedent (e.g., E.J (Pvt) Ltd v ZIMRA 19-HH-528) highlights that the courts often look at whether an activity is carried on “continuously or regularly.” If an activity is purely private or a hobby, it falls outside the scope of “trade” and thus cannot be standard rated.

Differentiating Tax Treatments

It is critical to distinguish between the three treatments, as they impact the registered operator’s ability to claim input tax:

| Treatment | Tax Rate | Input Tax Deduction |

| Standard Rated | Fixed % | Allowed (subject to compliance) |

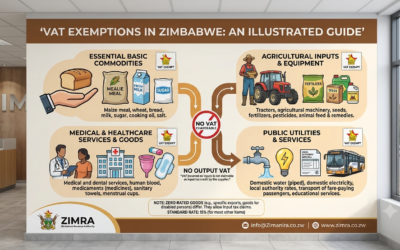

| Zero-Rated (Section 10) | 0% | Allowed |

| Exempt (Section 11) | N/A | Not Allowed |

Note: The distinction is vital for cash flow. If a business only makes exempt supplies, it cannot claim input tax deductions, effectively making the VAT paid on purchases a direct cost.

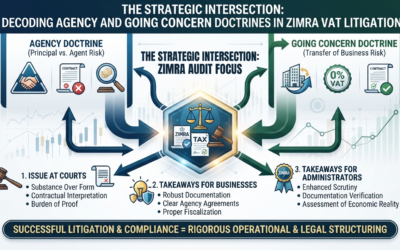

The Role of Case Law

The provided text contains valuable annotations regarding how Zimbabwean courts interpret the Act. These cases function as “red flags” or guidance points for compliance:

- Interpretation of “Trade” and “Supply”:

- Mylo (Pvt) Ltd v Zimra 16-HH-717: Broadens the concept of “supply” to include fulfilling a deficiency or want, which can capture barter transactions.

- E.J (Pvt) Ltd v ZIMRA 19-HH-528: Clarifies that trading in property, even if done as part of liquidation or winding up, can still be viewed as a supply in the course of trade.

- Zero-Rating Complications:

- Travel Agents (T(Pvt) Ltd v ZIMRA 15-HH-285): Highlights that services performed by travel agents on behalf of passengers are vatable services and not necessarily exempt.

- G (Pvt) Ltd v Zimra 22-HH-011: Emphasizes that for zero-rating under Section 10(2)(l) (services to non-residents), the requirements are cumulative; failure to meet one invalidates the zero-rating.

- The “Going Concern” Doctrine:

- MMI (Pvt) Ltd v The Commissioner General Zimra 19-HH-700: Discusses the nuances of property rights and the disposal of trade as a going concern.

Key Legislative Observations

- Fiscalisation (Section 2 & 20): The Act has evolved to include stringent requirements for fiscal devices. A tax invoice is no longer just a document; it must be a “fiscal tax invoice” generated by a compliant device and validated via the FDMS portal.

- Deemed Supplies (Section 7): The Act includes “deeming” provisions that create tax liabilities even where no traditional sale occurs (e.g., repossession of goods under an instalment credit agreement, or the personal use of business assets).

- Valuation (Section 3 & 9): The “Open Market Value” is the anchor for valuation, especially between connected persons. If you sell to a connected person for less than market value, the Commissioner may deem the consideration to be the open market value.

Compliance Requirements

To maintain compliance with Chapter 23:12, a taxpayer must ensure:

- Registration: Verification of the “registered operator” status.

- Invoicing: Use of fiscal devices for all standard-rated supplies.

- Documentation: Retention of proof for zero-rated supplies (Section 10(3)).

- Input Tax Control: Careful segregation of exempt vs. taxable supplies to ensure correct input tax apportionment under Section 16.