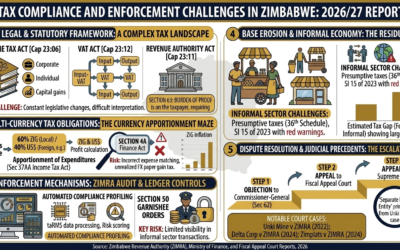

Zimbabwean Tax Deeming Provisions Explained!

Zimbabwean Tax Deeming Provisions Explained!

To understand these provisions, we must look at the three pillars of Zimbabwean taxation: the Income Tax Act, the Value Added Tax (VAT) Act, and the Capital Gains Tax (CGT) Act.

1. The Income Tax Act [Chapter 23:06]

Zimbabwe uses a source-based tax system. This means you are generally only taxed on money you earn from a source within Zimbabwe. However, the “Deeming Provisions” in Section 12 and Section 10 of the Income Tax Act extend this reach globally in specific scenarios.

Deemed Source (Section 12)

Imagine a Zimbabwean consultant who travels to Zambia for two weeks to fix a machine. Technically, the work happened in Zambia. However, under Section 12, if that work was done “in the course of a trade carried on in Zimbabwe,” the law deems that income to be from a Zimbabwean source.

Common examples of “Deemed Source” include:

-

Services Rendered Abroad: If you are a Zimbabwean resident and you go abroad to do work for your local employer, the salary you earn is deemed to be from a Zimbabwe source.

-

Interest on Loans: If you lend money to someone in Zimbabwe, the interest they pay you is deemed to be from a Zimbabwe source, even if the actual “contract” was signed in London.

-

Royalties: If you own a patent and a Zimbabwean company pays you to use it, that income is deemed to be from Zimbabwe.

Deemed Accruals (Section 10)

Sometimes, money hasn’t actually landed in your bank account, but the law says it has “accrued” to you. For instance:

-

Partnerships: A partner is deemed to have received their share of the profits the moment the partnership earns them, even if the cash is kept in the business for growth.

-

Income of Minor Children: If a parent moves assets into a child’s name to avoid higher tax brackets (income splitting), the law deems that income to still belong to the parent.

2. The Value Added Tax (VAT) Act [Chapter 23:12]

In the VAT system, deeming provisions focus on transactions. VAT is triggered by a “supply” of goods or services. But what if there is no sale?

Deemed Supplies (Section 7)

The VAT Act creates “Deemed Supplies” to ensure that the tax chain isn’t broken when goods are moved or used without a traditional sale.

-

Personal Use of Business Assets: If a shop owner takes a television from their stock to use at home, the law deems this to be a sale to themselves. They must account for VAT on the value of that TV.

-

Cessation of Trade: If a business closes down, any remaining stock or assets are “deemed” to have been sold at their market value on the day the business closed. This prevents people from claiming back VAT on purchases and then “vanishing” with the goods.

-

Insurance Indemnity Payments: When an insurance company pays out for a stolen business vehicle, the law deems that payout to be a “supply” made by the business. The business must then pay VAT on that insurance money.

3. The Capital Gains Tax (CGT) Act [Chapter 23:01]

Capital Gains Tax applies when you sell a “specified asset” (like a house or shares) for more than you bought it for. Deeming provisions here are used to prevent people from “giving away” assets to avoid tax.

Deemed Sales and Fair Market Value (Section 14)

If you sell a house to your brother for $1.00 just to avoid the 20% tax on the profit, the Zimbabwe Revenue Authority (ZIMRA) will step in. Under Section 14, the Commissioner is empowered to deem the sale to have happened at the Fair Market Value.

Deemed Control and Indirect Transfers

A significant update in recent years (and the 2026 Finance Act updates) involves Land-Holding Entities.

-

Indirect Disposals: If you don’t sell the land, but instead sell the shares of the company that owns the land, the law now deems this to be a sale of the land itself.

-

Offshore Deeming: Even if the share transfer happens between two companies in Dubai, if the underlying asset is Zimbabwean land, it is deemed to be a taxable event in Zimbabwe.

Why These Provisions Matter

Without deeming provisions, the tax system would be full of “holes.”

-

Fairness: It ensures that two people in the same economic position pay the same tax, regardless of how they structure the deal.

-

Anti-Avoidance: It stops taxpayers from using clever legal loopholes (like “gifts” or “offshore contracts”) to hide the true nature of their income.

-

Clarity: While “deeming” sounds complex, it actually provides a set of rules that tell you exactly when the taxman will show up, even if no cash has changed hands.

Summary Table: Deeming at a Glance

| Act | What is Deemed? | Layman’s Example |

| Income Tax | The Source | Working in Zambia for a Zim company; the money is “Zim money.” |

| VAT | The Supply | Taking business stock for home use; the law treats it as a “sale.” |

| CGT | The Price/Asset | Selling a house to a friend for cheap; tax is paid on the “real” value. |

Understanding these provisions is the difference between a “surprise tax bill” and a well-planned financial strategy. In Zimbabwe, the law doesn’t just look at what you did; it looks at what it deems you to have done.