In Zimbabwe, a trust is often viewed as a complex legal maze reserved for the wealthy. In reality, it is a practical tool used by many to protect family assets and manage inheritance. However, because a trust is a “person” in the eyes of the taxman, understanding its tax obligations is vital to avoid unwanted penalties from the Zimbabwe Revenue Authority (ZIMRA).

1. What is a Trust?

Think of a trust as a legal “container.” Instead of owning property (like a house, farm, or shares) in your own name, you place it inside this container.

-

The Founder (Settlor): The person who creates the trust and puts the assets into it.

-

The Trustees: The “managers” who look after the container. They don’t own the assets personally; they hold them for others.

-

The Beneficiaries: The people (usually family or a charity) who get to enjoy the “fruits” of the container, such as rental income or living in the trust’s house.

2. Formation and Types of Trusts

How is it formed?

In Zimbabwe, a trust is created through a document called a Trust Deed.

-

Drafting: A legal practitioner (usually a Notary Public) drafts the deed.

-

Registration: The deed is registered with the Registrar of Deeds (located in Harare or Bulawayo).

-

Transfer of Assets: Once registered, you must physically transfer assets (like changing the name on a Title Deed) into the name of the Trust.

Common Forms of Trusts

-

Family (Inter-vivos) Trust: Set up while the founder is still alive. It’s popular for protecting wealth across generations.

-

Testamentary Trust: Created via a person’s Will. It only “wakes up” after the person passes away.

-

Charitable Trust: Set up for non-profit goals. These can often apply for tax-exempt status from ZIMRA.

3. How is a Trust Taxed?

ZIMRA treats a trust as a separate taxpayer.

-

Tax Rate: Trusts are taxed at a flat rate of 25% plus a 3% AIDS Levy, making the effective rate 25.75%.

-

Filing Returns: Every trust is required to register for a Business Partner (BP) number and submit an annual tax return (ITF 12), even if it didn’t make a profit that year.

-

Capital Gains Tax (CGT): If a trust sells a “specified asset” (like a house or shares), it pays CGT—typically 20% on the profit for assets acquired after February 2009.

4. Who Pays the Tax? (The Distribution Rule)

One of the most common questions is: Does the trust pay, or do the people getting the money pay? In Zimbabwe, it depends on whether the money stays in the “container” or is given out.

| Scenario | Who is Taxable? |

| Income stays in the Trust | The Trust pays tax at the 25.75% flat rate. |

| Income is given to Beneficiaries | The Beneficiaries are taxed on what they received. |

| Income for Minor Children | If a founder gives money to their minor child through a trust, the Founder may be taxed (this prevents people from using kids to hide income). |

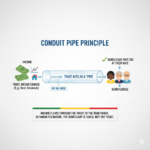

5. The “Conduit Pipe” Principle

This is the golden rule of trust taxation. Imagine the trust is not a solid box, but a hollow pipe.

If the trust receives income (e.g., $1,000 in rent) and immediately passes it to a beneficiary in the same tax year, the trust is treated as a “conduit” (a pipe).

-

The Flow: The money flows through the trust to the beneficiary.

-

Nature of Income: The money keeps its “identity.” If the trust received it as a dividend, the beneficiary is treated as having received a dividend.

-

Tax Benefit: Because the money didn’t “stop” in the trust, the trust doesn’t pay tax on it. The beneficiary pays tax at their own individual rate, which might be lower than the trust’s flat 25.75%.

6. Important 2026 Updates

As of January 1, 2026, Zimbabwe has introduced several changes that affect trusts:

-

VAT Increase: If your trust is registered for VAT (e.g., it runs a commercial business), the standard rate has increased to 15.5%.

-

Rental Withholding Tax: There is a new 10% withholding tax on rental income. If your trust earns rent from a company, that company might be required to deduct 10% and pay it directly to ZIMRA on the trust’s behalf.

-

IMTT: The tax on electronic transfers in local currency (ZiG) has been reduced to 1.5%, while USD remains at 2%.

Summary Note: While trusts are excellent for avoiding the “Estate Duty” (the 5% tax paid when a person dies), they are not a “get out of tax free” card. They require careful accounting and annual filings to stay on the right side of ZIMRA.