Income Tax return (ITF12C) Deadline – The April 30th Countdown

As Zimbabwe approaches the 30 April 2026 deadline for the 2025 Year of Assessment, the accounting profession is grappling with a “dual-reality” economy. On one hand, the Zimbabwe Gold (ZiG) has completed its first full year of circulation; on the other, the US Dollar (USD) continues to dominate transactional volume. For accountants using ZIMRA’s Tax and Revenue Management System (TaRMS), the technical ease of reporting in both currencies masks a deeper accounting challenge: What is the official reporting currency for 2025 Financial Statements?

1. The 2025 Monetary Policy Statement: The “Presentation” Mandate

The most significant shift in the 2025 reporting cycle came from the Reserve Bank of Zimbabwe (RBZ) on 6 February 2025. While the 2024 PAAB Heatmap focused on the technicalities of converting old ZWL balances, the 2025 MPS moved toward standardizing the output.

The Key Directive:

The RBZ, in consultation with the PAAB, mandated that all entities in Zimbabwe adopt a uniform presentation currency, specifically the ZiG, for their financial statements.

Why this matters:

In IFRS terms (specifically IAS 21), there is a distinction between:

- Functional Currency: The currency of the primary economic environment in which the entity operates (often USD for Zimbabwean firms).

- Presentation Currency: The currency in which the financial statements are presented (now mandated as ZiG).

The 2025 MPS essentially stripped away the “choice” of presentation currency. Even if your business is 90% USD-functional, your primary set of Financial Statements for the 2025 year must be presented in ZiG to ensure “comparability across the economy.”

2. Functional vs. Presentation: The IAS 21 Tug-of-War

The 2024 PAAB Heatmap correctly stated that functional currency is “entity-specific and cannot be externally prescribed.” The 2025 MPS does not contradict this, but it adds a layer of complexity.

If your Functional Currency is USD:

You still measure your transactions in USD throughout the year. However, for the 2025 year-end, you must translate those USD figures into ZiG. According to IAS 21:

- Assets and Liabilities are translated at the closing rate (the interbank mid-rate as of 31 December 2025).

- Income and Expenses are translated at the exchange rates at the dates of the transactions (or an appropriate average rate).

- Resulting exchange differences are recognized in Other Comprehensive Income (OCI).

If your Functional Currency is ZiG:

You are subject to IAS 29 (Financial Reporting in Hyperinflationary Economies). Despite the relative stability noted in the mid-2025 MPS Review, the cumulative 3-year inflation (including the ZWL spike in early 2024) means most auditors still require IAS 29 restatements for ZiG-functional entities in 2025.

3. TaRMS and ZIMRA: The Practical Reality

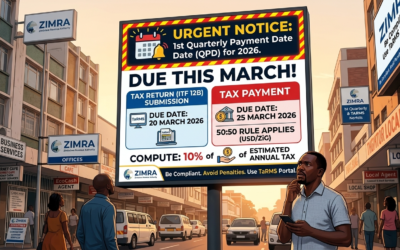

ZIMRA’s TaRMS platform is designed to be “currency-agnostic,” but it operates under the legal framework of Statutory Instrument 81 of 2025. This creates a specific workflow for the April 30th deadline:

- The 50/50 Rule: For the 2025 period, if your income is earned in both currencies, TaRMS requires you to declare the specific portions. If your foreign currency income exceeds 50%, you pay 50% of your tax in USD and 50% in ZiG.

- The Base Currency: While you enter both currencies, TaRMS aggregates the data. Most tax practitioners are finding that for the ITF 12C (Income Tax Return), the system expects a consolidated view that aligns with the ZiG-denominated Financial Statements mandated by the MPS.

- Exchange Rate Consistency: ZIMRA requires the use of the Willing-Buyer Willing-Seller (WBWS) rate. Any discrepancy between the rate used in your Financial Statements (per IAS 21) and the rate used on TaRMS can lead to “unexplained tax variances” during an audit.

4. Is the 2024 Heatmap Still “Safe”?

The 08-10-2024 Heatmap remains a vital technical guide for the initial conversion logic. However, it is no longer the only guide.

What has changed since the Heatmap:

- Hyperinflation Assessment: The Heatmap said it was “premature” to judge. By the end of 2025, the RBZ reported annual inflation dissipating to 15% (by December 2025). This creates a conflict: the qualitative indicators of IAS 29 (preference for USD) remain, but the quantitative indicator (3-year cumulative) is starting to trend downward.

- The Presentation Mandate: The Heatmap allowed for more flexibility in reporting currency than the 2025 MPS now permits.

5. Audit Risks and “Faithful Representation”

The move to a mandated ZiG presentation currency has raised concerns among Chartered Accountants regarding “Faithful Representation.” If a company operates entirely in USD, translating to ZiG might distort the financial reality if the exchange rate does not reflect true market parity.

Recommendation for the 2025 Return:

- Dual Presentation: Many firms are choosing to present “Convenience Translations.” They produce the mandated ZiG accounts for the regulator/ZIMRA, but provide USD-functional accounts as supplementary information for shareholders.

- Explicit Disclosure: Your “Basis of Preparation” note in the 2025 Financial Statements must explicitly state that ZiG is the presentation currency as mandated by the RBZ, and clearly define the functional currency.

The Road to April 30

The 2025 tax season is the first “true” test of the ZiG’s integration into formal accounting. To be compliant:

- Respect the Mandate: Use ZiG as your presentation currency in the main Financial Statements.

- Apply the Law: Follow SI 81 of 2025 for the 50/50 tax split on TaRMS.

- Document Everything: Ensure your IAS 21 translation gains/losses are clearly calculated, as ZIMRA often scrutinizes these “non-cash” items.