Income Tax Currency Split Analysis and 2025 ITF12C

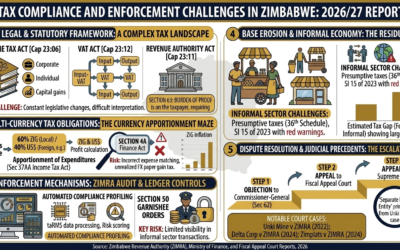

For the Zimbabwean business community, 2024 was a year of profound fiscal transition, marked by the introduction of the Zimbabwe Gold (ZiG) and a fundamental shift in how the Zimbabwe Revenue Authority (ZIMRA) views the currency of tax settlement. Public Notice 99 of 2024, issued in late 2024, solidified a trend that now dictates the 2025 tax landscape: the mandatory 50-50 currency split for multi-currency earners. This article analyzes the legislative underpinnings of this shift and provides a roadmap for accurate ITF12C self-assessment in 2025.

The Legislative Evolution: From Section 4A to the 50-50 Mandate

Traditionally, Section 4A of the Finance Act [Chapter 23:04] required taxpayers to pay tax in the currency of trade. If you earned USD, you paid USD; if you earned local currency, you paid local currency. However, the economic need to bolster the local currency led to a legislative “intervention” via the Finance Act, 2024 (No. 2 of 2024).

The Key Amendment

The Finance Act amended Section 4A to introduce a threshold-based rule. With effect from 1 July 2024, and continuing into the 2025 year of assessment:

- The 50% Threshold: If a person (individual or corporate) receives more than 50% of their total income in foreign currency, they must account for tax as if exactly half (50%) of that income was earned in foreign currency and the other half in local currency.

- Proportionate Rule: If foreign currency income is 50% or less of total income, the taxpayer remains on the “Proportionate to Trade” basis (paying in the exact ratio of their actual earnings).

Dive into Public Notice 99 of 2024

Public Notice 99 was the operational directive that clarified how this legislative amendment should be applied during the transition. It broke down the 2024 QPD cycles into distinct phases:

- Q1: Purely proportionate.

- Q2: Optional 50-50 or proportionate.

- Q3 & Q4: Mandatory 50-50 for those exceeding the 50% forex threshold.

Why this matters for 2025

While Public Notice 99 focused on the 2024 4th QPD, it set the precedent for the 2025 Year of Assessment. For the ITF12C return due for 2025, businesses must apply these rules to their total annual income. ZIMRA’s stance is clear: the “deeming” provision—treating half your income as local currency—is not just an option; it is a statutory requirement for high-forex earners.

Applying the Split in the ITF12C for 2025

The ITF12C (Income Tax Self-Assessment Return) requires a meticulous breakdown. When preparing your 2025 return, you cannot simply report one total figure. You must follow the “Two-Column” approach.

Step 1: Consolidation and Comparison

First, convert all foreign currency income to local currency (ZiG) using the official exchange rate to determine your ratio.

- Total Income (Converted to ZiG) / Forex Income (Converted to ZiG).

- If this ratio is > 50%, you move to the mandatory 50-50 split calculation.

Step 2: The Deeming Calculation

Under the 50-50 rule, even if your actual revenue was 90% USD and 10% ZiG, for tax purposes, you will:

- Calculate total taxable income in a single currency (e.g., ZiG).

- Divide the resulting tax liability by two.

- Pay one-half in USD (using the rate at the date of payment) and one-half in ZiG.

Step 3: Handling Expenses

A common pitfall is the apportionment of expenses. Public Notice 99 emphasizes that expenses must also be apportioned to the respective currency streams. If you are on a 50-50 split for income, your allowable deductions should generally follow a rational apportionment to ensure you aren’t over-claiming in one currency to “wipe out” the tax liability of another.

Risks and Penalties

The 2025 National Budget introduced stricter enforcement measures.

- Late Submission: The penalty for late submission of returns has been reviewed upward to US$30 per day.

- Currency Non-Compliance: Failing to pay in the correct currency split is viewed as a “shortfall” in that specific currency, attracting interest and 100% penalties on the “unpaid” portion of the specific currency, even if you overpaid in the other.

- TaRMS Integration: The Tax and Revenue Management System (TaRMS) is now configured to track payments against specific currency obligations.

Conclusion for Businesses

Public Notice 99 and the subsequent Finance Acts represent a shift toward “Deemed Local Currency Trade.” For 2025, the strategy is no longer just about tracking what you earned, but actively monitoring your Forex vs. ZiG ratio.

Businesses should:

- Update accounting software to track transactions by currency of origin.

- Perform quarterly “Ratio Audits” to see if they cross the 50% threshold.

- Ensure that provisional tax (QPDs) throughout 2025 already reflects this 50-50 split to avoid a massive “wash-up” payment and interest when the ITF12C is filed in 2026.

By mastering the 50-50 split today, your business ensures compliance and avoids the heavy-handed penalties of a ZIMRA audit in the coming year.

The Decision Matrix for 2025

Your settlement method depends entirely on your revenue composition:

| Scenario | Revenue Mix | Settlement Method |

| Dominant Forex | > 50% USD Earnings | 50-50 Split Rule: 50% of total tax in USD, 50% in ZiG. |

| Dominant Local | ≥ 50% ZiG Earnings | Proportionate Rule: Tax settled in the exact ratio of trade. |

Impact on ITF12C Filings

When preparing the 2025 ITF12C, businesses must perform a “shadow” consolidation:

- Step A: Aggregate all income into a single reporting currency (usually ZiG) using the prevailing mid-market rates for calculation purposes.

- Step B: Allocate deductions. Note that expenses incurred in a specific currency should generally be deducted from income in that same currency to maintain tax neutrality.

- Step C: Calculate the Total Annual Tax (24% Corporate Tax + 3% AIDS Levy).

- Step D: Apply the PN 99/2024 split logic to determine the final USD vs. ZiG liability.

Critical Risks

- Underestimation: If you settle on a proportionate basis but your year-end audit shows your USD income crossed the 50% mark, you may be liable for interest on the “missing” USD portion of the 50-50 split.

- Currency Matching: Ensure that QPDs paid during the year are correctly credited against the respective currency buckets in the TaRMS system.

Recommendation:

Finance teams should perform a quarterly “Stress Test” on the revenue mix. If your USD revenue is hovering around 45-55%, it is safer to adopt the 50-50 split early to avoid a significant USD cash flow shock during the 4th QPD or final return.