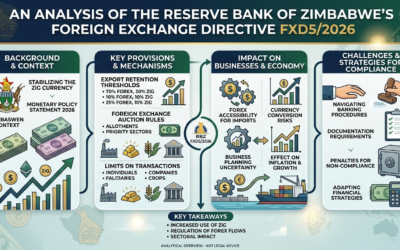

The Reserve Bank of Zimbabwe (RBZ), through the 2026 Monetary Policy Statement and the specific Exchange Control Directive FXD5/2026, has signaled a paradigm shift in the nation’s de-dollarization trajectory. Moving away from the rigid 2030 deadline previously set, the central bank has adopted a “Conditions Precedent” (CP) framework. This framework posits that the transition to the Zimbabwe Gold (ZiG) as the sole legal tender will not be a result of administrative fiat, but a market-driven outcome contingent upon the satisfaction of specific economic benchmarks.

The Reserve Bank of Zimbabwe (RBZ), through the 2026 Monetary Policy Statement and the specific Exchange Control Directive FXD5/2026, has signaled a paradigm shift in the nation’s de-dollarization trajectory. Moving away from the rigid 2030 deadline previously set, the central bank has adopted a “Conditions Precedent” (CP) framework. This framework posits that the transition to the Zimbabwe Gold (ZiG) as the sole legal tender will not be a result of administrative fiat, but a market-driven outcome contingent upon the satisfaction of specific economic benchmarks.

This article explores the five pillars of the FXD5/2026 roadmap: sustained low inflation, adequate foreign reserve cover, exchange rate efficiency, fiscal-monetary congruence, and financial system resilience.

1. Introduction: From Deadlines to Data

For decades, Zimbabwe’s monetary landscape has been characterized by a multi-currency system, primarily dominated by the United States Dollar (USD). While providing a temporary anchor for price stability, the reliance on a foreign currency has limited the RBZ’s ability to conduct independent monetary policy and has exposed the economy to external shocks.

The introduction of the ZiG in 2024 marked the beginning of a “Back to Basics” approach. However, as of early 2026, the Governor of the RBZ, Dr. John Mushayavanhu, has clarified that the “when” of mono-currency is less important than the “how.” Directive FXD5/2026 formalizes this by listing the “Conditions Precedent”—the objective economic realities that must be present before the economy can safely abandon the USD.

2. Pillar I: Sustained Single-Digit Inflation

The most critical condition precedent cited in FXD5/2026 is the attainment and maintenance of single-digit annual inflation.

The Milestone of January 2026

In January 2026, Zimbabwe achieved a historic milestone: local currency inflation dropped to 4.1%, the first time in over three decades. This was a drastic reduction from the peak levels of 95.8% seen in July 2025.

The CP Requirement

Under FXD5/2026, the RBZ requires this stability to be “durable.” A single month or quarter of low inflation is insufficient. The central bank’s strategy involves:

- Prudent Money Supply Management: Ensuring that the growth of ZiG in circulation is strictly aligned with real economic activity.

- Inflation Expectations: Anchoring the public’s belief that prices will remain stable, thereby preventing the “forward-pricing” behavior that plagued previous iterations of the local currency.

3. Pillar II: Adequate Foreign Reserve Buffers

A sovereign currency is only as strong as the assets that back it. FXD5/2026 emphasizes the build-up of foreign reserves as a defensive mechanism against speculative attacks.

The Import Cover Benchmark

The directive sets a specific target: three to six months of import cover.

- Current Status: As of February 2026, reserves stood at approximately US$1.2 billion, representing roughly 1.5 months of import cover.

- The Logic: In a mono-currency environment, the central bank must have the capacity to intervene in the market to provide liquidity for essential imports (medicine, fuel, grain) without causing a spike in the exchange rate.

FXD5/2026 maintains the 70% foreign currency retention threshold for exporters, ensuring a steady stream of “surrender” proceeds that the RBZ uses to build these reserves.

4. Pillar III: Efficient and Transparent Exchange Rate System

A successful transition to a mono-currency requires a market-determined exchange rate that reflects the true value of the currency.

The Willing-Buyer Willing-Seller (WBWS) Model

FXD5/2026 continues to refine the WBWS interbank market. The goal is to eliminate the “black market premium.”

- Market Discovery: By allowing banks to trade foreign currency freely within regulated margins (removing the previous 5% cap), the RBZ ensures that the ZiG price is discovered through demand and supply.

- Indifference Principle: Governor Mushayavanhu has stated that the ultimate test of this CP is when the public is “indifferent” to whether they are paid in USD or ZiG. This indifference only occurs when the official rate is credible and accessible.

5. Pillar IV: Fiscal and Monetary Policy Congruence

History has shown that monetary stability in Zimbabwe is often undermined by fiscal indiscretion. FXD5/2026 is supported by a government pledge to “stop the printing press.”

Eliminating Central Bank Financing

A core condition for mono-currency is the strict adherence to a “no-overdraft” policy at the central bank.

- Fiscal Rectitude: The Ministry of Finance must fund its requirements through tax revenue and the issuance of market-based bonds, rather than borrowing from the RBZ.

- Mutually Reinforcing Policies: When the Treasury maintains a surplus or a manageable deficit and the RBZ maintains tight liquidity, the resulting stability provides the foundation for the ZiG to stand alone.

6. Pillar V: Safe, Sound, and Digitalized Financial Systems

The final condition involves the infrastructure of the economy. For the ZiG to be the sole currency, the payment systems must be robust enough to handle 100% of the nation’s transaction volume.

Digitalization and Payment Stability

- Upward Revision of Limits: To encourage ZiG usage, FXD5/2026 and the 2026 MPS increased withdrawal and mobile money transaction limits.

- Resilience: The financial sector must be capitalized and “digital-first” to ensure that electronic payments are seamless, reducing the psychological need for physical USD cash.

7. Implications of FXD5/2026 for Business and Investors

For the private sector, FXD5/2026 provides a predictable roadmap. Businesses are no longer guessing when the change will happen; they can now monitor the data to see if the change is approaching.

- Interest Rate Stability: With the Bank Policy Rate maintained at 35% in early 2026, the RBZ is signaling that it will keep borrowing costs high until the CPs are firmly met.

- Savings Culture: The introduction of ZiG-denominated term deposits aims to rebuild the savings culture that was destroyed during hyperinflation.

8. Conclusion: A Market-Led Evolution

The “Conditions Precedent” approach outlined in FXD5/2026 represents a mature evolution in Zimbabwe’s monetary policy. By abandoning the 2030 deadline in favor of objective economic triggers, the RBZ has removed the “ticking clock” pressure that often leads to rushed, unsuccessful reforms.

The transition to a mono-currency in Zimbabwe is now an evidence-based journey. If the progress made in 2025—characterized by 4.1% inflation and growing gold reserves—can be sustained through 2026 and 2027, the “indifference” required for a single-currency economy may arrive sooner than anyone anticipated. However, until the boxes for import cover and sustained stability are fully ticked, the dual-currency system remains a necessary bridge.

Reference: Reserve Bank of Zimbabwe, 2026 Monetary Policy Statement & Exchange Control Directive FXD5/2026.