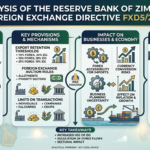

Navigating Stability: An Analysis of the Reserve Bank of Zimbabwe’s Foreign Exchange Directive FXD5/2026

The release of Foreign Exchange Directive FXD5/2026 by the Reserve Bank of Zimbabwe (RBZ) marks a pivotal moment in the nation’s ongoing monetary journey. Coming on the heels of the 2026 Monetary Policy Statement, the directive provides the granular legal and operational instructions required to implement the central bank’s “Stay the Course” strategy. After years of currency volatility, the RBZ is doubling down on a framework designed to protect the gains made by the Zimbabwe Gold (ZiG), which achieved a historic single-digit annual inflation rate of 4.1% in January 2026.

The release of Foreign Exchange Directive FXD5/2026 by the Reserve Bank of Zimbabwe (RBZ) marks a pivotal moment in the nation’s ongoing monetary journey. Coming on the heels of the 2026 Monetary Policy Statement, the directive provides the granular legal and operational instructions required to implement the central bank’s “Stay the Course” strategy. After years of currency volatility, the RBZ is doubling down on a framework designed to protect the gains made by the Zimbabwe Gold (ZiG), which achieved a historic single-digit annual inflation rate of 4.1% in January 2026.

This article provides a deep-dive analysis of FXD5/2026, breaking down its core policy measures, interpreting the regulatory intent, and assessing the multi-dimensional impact on businesses, consumers, and the broader financial landscape.

1. Maintenance of Exporter Foreign Currency Retention at 70%

The Policy Measure

Foreign Exchange Directive FXD5/2026 reaffirms that the foreign currency retention threshold for all exporters remains at 70%. Exporters are permitted to retain 70% of their export proceeds in their Foreign Currency Accounts (FCAs), while the remaining 30% must be liquidated into the domestic currency (ZiG) at the prevailing interbank market rate.

Interpretation

The RBZ is prioritizing “policy consistency.” By maintaining the 70/30 split, the central bank avoids the “shock therapy” of a sudden increase in surrender requirements, which often leads to side-marketing or under-invoicing. The 30% surrender portion is the lifeblood of the interbank market, providing the “Willing-Buyer Willing-Seller” (WBWS) system with the necessary liquidity to meet the demands of non-exporting importers (e.g., retailers and manufacturers of basic goods).

Impact

- On Exporters: The 70% retention allows miners and manufacturers to meet their offshore obligations—such as importing raw materials, machinery, and servicing external debt—without relying on the central bank for allocations. This fosters operational autonomy.

- On Market Liquidity: The 30% mandatory liquidation ensures a steady flow of USD into the interbank market. This prevents a “dry market,” which historically drove businesses to the parallel market to find foreign exchange.

- On Currency Stability: By ensuring that a portion of all export earnings is converted to ZiG, the RBZ creates natural demand for the local currency, helping to anchor its value against the USD.

2. Upward Revision of Cash Withdrawal and Transaction Limits

The Policy Measure

The directive introduces a significant increase in cash withdrawal limits. Individuals can now withdraw up to ZiG10,000 per week, while corporates are permitted up to ZiG100,000 per week. Furthermore, transaction limits for mobile money and ZIPIT platforms have been adjusted upward to align with the current price levels and the “Upgraded Big 5” banknote series.

Interpretation

This measure is a response to “liquidity friction.” For a local currency to be effective, it must be accessible and usable. By raising these limits, the RBZ is acknowledging that the previous ceilings were restrictive for a growing economy. It also facilitates the rollout of the new, higher-denomination ZiG banknotes (ZiG50, ZiG100, and ZiG200), ensuring that the physical currency circulation matches economic activity.

Impact

- Consumer Convenience: Higher limits reduce the frequency of bank visits and the “queue culture” that has plagued Zimbabwean banking. It makes the ZiG more practical for day-to-day transactions.

- Business Efficiency: For SMEs and informal traders who operate largely in cash, the ZiG100,000 corporate limit allows for smoother payroll and local procurement processes.

- Velocity of Money: Increased transactional limits boost the velocity of the ZiG within the formal system, discouraging the use of the USD for small-scale retail transactions.

3. Deepening the Willing-Buyer Willing-Seller (WBWS) Interbank Market

The Policy Measure

Directive FXD5/2026 mandates that all foreign exchange transactions for the procurement of goods and services must be conducted through the WBWS interbank market. Authorized Dealers (banks) are instructed to prioritize “genuine productive sector requirements.” It explicitly prohibits the use of borrowed ZiG funds to purchase foreign currency on the WBWS market.

Interpretation

The RBZ is moving toward an “indirect” monetary policy framework. Instead of the central bank setting the rate via an auction, the WBWS allows for market-driven price discovery. The prohibition on using borrowed funds for forex purchases is a crucial “anti-speculation” guardrail. It prevents businesses from taking out cheap ZiG loans to buy USD, a practice that historically led to currency “burning” and hyperinflation.

Impact

- Exchange Rate Discovery: The interbank rate becomes a more accurate reflection of supply and demand, reducing the “premium” between the official and parallel markets.

- Curbing Speculation: By cutting off the supply of credit for forex hoarding, the RBZ stabilizes the ZiG. Credit growth is funneled into production rather than currency arbitrage.

- Price Stability: A stable, market-determined exchange rate allows businesses to price their goods accurately in ZiG, preventing the constant “re-pricing” that fuels inflation.

4. Introduction of the ZiG Denominated Term Deposit Facility (ZIGDTDF)

The Policy Measure

A new instrument, the ZiG Denominated Term Deposit Facility, has been introduced. This facility allows banks to place excess ZiG liquidity with the Reserve Bank at attractive interest rates.

Interpretation

This is a classic “sterilization” tool. When there is too much ZiG in the system, it risks chasing too few USD, causing the local currency to depreciate. The ZIGDTDF incentivizes banks to lock away their ZiG instead of offloading it onto the foreign exchange market.

Impact

- Liquidity Management: The RBZ gains a surgical tool to mop up excess liquidity without resorting to draconian statutory reserve hikes.

- Bank Profitability: Commercial banks gain a low-risk avenue to earn interest on their ZiG holdings, which can help offset the costs of the Governor’s directive to lower bank charges.

- Savings Culture: If banks pass these rates on to customers, it could revitalize the domestic savings market, which is essential for long-term investment.

5. Regulatory Compliance and Enforcement (The “Stick”)

The Policy Measure

FXD5/2026 outlines strict penalties for non-compliance with exchange control regulations. Penalties include civil fines of 1% of the transaction value or USD 100,000 (equivalent), whichever is greater. It also reiterates the 90-day acquittal period for export receipts and import documentation.

Interpretation

The RBZ is signaling that “the era of laxity is over.” The heavy fines are designed to be a deterrent against “transfer pricing,” “mis-invoicing,” and the “externalization” of funds. The focus on documentation (acquittal) ensures that every dollar leaving the country is for a legitimate, verified purpose.

Impact

- Improved Transparency: Corporates are forced to maintain cleaner books and adhere to international best practices in trade finance.

- Reduced Illicit Flows: Strict monitoring of NRTAs (Non-Resident Transferable Accounts) and external loan registrations makes it harder for actors to syphon capital out of the country.

- Resource Mobilization: Better acquittal of export receipts ensures that the nation’s foreign currency earnings actually return to the domestic banking system, strengthening the balance of payments.

6. Strategic Shift: Conditions-Based Mono-Currency Transition

The Policy Measure

While not a single “clause,” FXD5/2026 operationalizes the strategic shift from a fixed “2030 De-dollarization Target” to a “Conditions-Based Framework.” The directive emphasizes that foreign exchange management will be guided by benchmarks: 3–6 months of import cover, sustained single-digit inflation, and exchange rate stability.

Interpretation

This is arguably the most significant psychological shift in the 2026 policy. By removing the “ticking clock” of 2030, the RBZ has reduced the speculative pressure that occurs when a deadline approaches. The directive signals to the market that the USD will remain legal tender until the ZiG is strong enough to stand on its own based on data, not dates.

Impact

- Market Confidence: Businesses can plan long-term investments without the fear of a “forced” currency changeover that they aren’t prepared for.

- FDI Attraction: Foreign investors are more comfortable entering a market where currency transition is governed by economic stability rather than political decree.

- Policy Flexibility: The RBZ retains the “optionality” to move faster or slower toward a mono-currency depending on global commodity prices and domestic agricultural performance.

Conclusion

Foreign Exchange Directive FXD5/2026 is a sophisticated regulatory instrument that balances the need for liquidity with the imperative of stability. It marks a transition from “crisis management” to “prudent stewardship.” By maintaining high retention for exporters, curbing speculative borrowing, and introducing market-based instruments like the ZIGDTDF, the RBZ is attempting to build a sustainable monetary foundation.

However, the success of these measures depends heavily on the “Coordination Principle”—the synergy between the RBZ’s monetary discipline and the Treasury’s fiscal discipline. If the government continues to adhere to its “no borrowing from the central bank” pledge, the measures in FXD5/2026 provide a credible roadmap toward a stable, prosperous, and eventually mono-currency Zimbabwean economy.