Navigating Zimbabwe’s Foreign Exchange Framework: Free Funds, Retention, and Liquidation

Introduction

In the evolving landscape of Zimbabwe’s financial ecosystem, understanding the mechanics of foreign exchange is not merely an administrative requirement—it is a critical necessity for businesses and individuals alike. The Reserve Bank of Zimbabwe (RBZ) provides the regulatory framework that governs how foreign currency enters, circulates, and exits the domestic economy.

Central to these regulations are three interconnected concepts: the status of “Free Funds,” the mandatory export surrender (liquidation) requirement, and the retention of export proceeds. This article demystifies these components, drawing on the latest regulatory guidelines to provide clarity on how these rules shape the daily operations of traders, exporters, and the general public.

Defining “Free Funds”

The term “Free Funds” is frequently used in Zimbabwean financial discourse, but it carries a specific legal definition that distinguishes it from general foreign currency earnings.

The Legal Definition

According to the Exchange Control Regulations, specifically Statutory Instrument 109 of 1996 and referenced in subsequent updates, “Free Funds” are defined as:

“Money which is lawfully held outside Zimbabwe by a Zimbabwean resident and which was acquired by him otherwise than as the proceeds of any trade, business or other gainful occupation or activity carried on by him in Zimbabwe.”

Key Characteristics

To qualify as “Free Funds,” the source is the deciding factor. Unlike export proceeds, which are generated through the sale of goods or services from within Zimbabwe, Free Funds typically originate from:

- Diaspora Remittances: Funds sent by Zimbabweans living abroad to family or individuals back home.

- Consultancy Earnings: Income earned by individuals from foreign entities for services rendered externally.

- Salaries: Foreign currency wages paid by an employer, provided they do not constitute proceeds from domestic trade that would otherwise be subject to surrender requirements.

- Donations and Gifts: Inward flows from international organizations or private donors.

Why the Distinction Matters

The “Free” in Free Funds implies a high level of liquidity and usage flexibility. Holders of Free Funds (individuals, Embassies, NGOs, and International Organizations) are permitted to use their balances for both domestic and foreign obligations without the same restrictive liquidation requirements applied to corporate exporters. They are effectively treated as 100% available to the account holder.

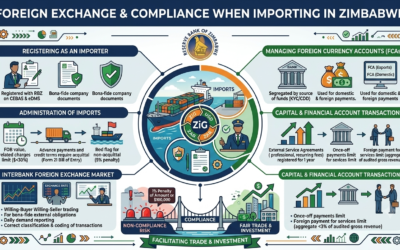

Export Proceeds: The 70/30 Rule

For corporate entities and exporters, the regulatory framework is different. When a business exports goods or services, the resulting foreign currency earnings are subject to the RBZ’s surrender and retention framework. This framework is designed to balance the country’s need for foreign currency reserves with the operational needs of the private sector.

The Mechanics of the Split

As per the current Foreign Exchange Transactions Guidelines, the distribution of gross export receipts is dictated by a split between the portion that must be sold to the Reserve Bank (liquidation) and the portion that can be kept by the exporter (retention).

The formula for this distribution can be expressed as follows:

Let G be the Gross Export Receipts.

The Retention Amount (R) and the Liquidation Amount (L) are calculated as:

R = G times 0.70L = G times 0.30Under current policy:

- 70% Retention: The exporter is permitted to retain 70% of their gross export receipts in their Foreign Currency Account (FCA). These funds can be held indefinitely to fund their own operational imports, external obligations, or other business needs.

- 30% Liquidation: 30% of the gross export receipts must be surrendered (liquidated) to the RBZ at the prevailing interbank exchange rate.

Exceptions to the Rule

The standard 70/30 split is not universal. The RBZ enforces a compliance-based adjustment for exporters who fail to comply with regulations.

If an exporter has overdue export proceeds (i.e., they have failed to acquit export documentation within the stipulated timeframes), the surrender requirement increases:

L_overdue = G times 0.50R overdue = G times 0.50

In this scenario, the liquidation requirement jumps to 50%, significantly reducing the retained portion to 50%. This serves as a strong regulatory incentive for exporters to ensure their export documentation (CD1 forms, etc.) is acquitted timeously.

The Liquidation Process Explained

The “30% Liquidation Rule” is often misunderstood as a penalty. In reality, it is a mechanism for central bank liquidity management. Here is how the process functions within the banking system:

The Interbank Mechanism

When an exporter receives payment for goods or services from offshore, the funds land in their “Corporate FCA (Exports).” The Authorized Dealer (the commercial bank) is responsible for ensuring that the surrender requirement is met.

- Calculation: Upon credit of the funds, the bank calculates the 30% surrender value.

- Conversion: The bank sells this 30% portion into the interbank foreign exchange market at the prevailing market-determined exchange rate.

- Settlement: The local currency equivalent is credited to the exporter’s local currency account, while the remaining 70% remains in the exporter’s FCA as foreign currency.

Why This Mechanism Exists

The RBZ utilizes this surrender mechanism to ensure that the interbank market has sufficient foreign currency liquidity to support importers who may not have their own export proceeds. This facilitates the “Willing-Buyer-Willing-Seller” model, aiming to promote market stability and ease of access to foreign currency for bona fide external payments.

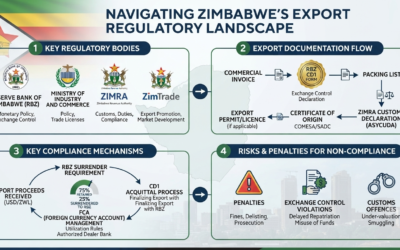

Compliance and Monitoring

The adherence to these rules is monitored through the Computerized Export Payments Exchange Control System (CEPECS) and other reporting systems.

Responsibilities of Authorized Dealers

Commercial banks act as the front-line enforcers of these guidelines. They are required to:

- Exercise “Know Your Customer” (KYC) and “Customer Due Diligence” (CDD) principles.

- Flag non-compliant exporters (those with overdue proceeds).

- Report inflows and outflows accurately to the Reserve Bank for Balance of Payments (BOP) tracking.

Penalties for Non-Compliance

Failure to comply with these guidelines can lead to being “red-flagged” in the CEPECS system. Being red-flagged often results in:

- Increased administrative penalties.

- Heightened scrutiny of all foreign exchange transactions.

- Restrictions on the ability to conduct further business until the outstanding export documentation is regularized.

Conclusion

Zimbabwe’s foreign exchange framework is designed to facilitate trade while maintaining national monetary stability. Understanding the distinction between “Free Funds” and “Export Proceeds” is the foundation of navigating these regulations.

While the 70% retention policy offers exporters a degree of autonomy in managing their foreign currency, the 30% liquidation requirement remains a vital component of the country’s macroeconomic strategy. For any business operating in this environment, meticulous record-keeping, timely acquittal of export forms, and a clear understanding of these thresholds are essential to avoiding unnecessary compliance bottlenecks.

Disclaimer: This article is for educational purposes and is based on the provided Foreign Exchange Transactions Guidelines. Regulatory policies in Zimbabwe are subject to change by the Reserve Bank; businesses should always consult their Authorized Dealers or the latest RBZ circulars for the most current directives.