A Comprehensive Legal and Financial Analysis of the Twelve Withholding Tax (WHT) Returns in Zimbabwe

1. The Paradigm of Source-Based Withholding Taxation in Zimbabwe

Withholding tax (WHT) is an administrative mechanism designed to collect tax at the point of payment or transaction. Rather than relying on the taxpayer to declare and pay tax at the end of a tax year, the legislature mandates a “withholding agent” to deduct the tax at source and remit it directly to the Zimbabwe Revenue Authority (ZIMRA). In Zimbabwe, this regime is governed primarily by the Income Tax Act [Chapter 23:06], the Capital Gains Tax Act [Chapter 23:01], and the Finance Act [Chapter 23:04].

Withholding taxes serve three primary purposes in the Zimbabwean fiscal environment:

- base protection, ensuring that non-residents and informal traders who operate outside the standard corporate tax net still contribute to the fiscus;

- cash flow normalization, providing the state with consistent monthly revenues; and

- administrative efficiency, reducing the cost of tax collection by shifting the burden of collection, record-keeping, and remittance onto private business entities.

The implementation of the Tax Revenue Management System (TaRMS) has further centralized these returns under the Single Business Account (SBA) architecture. However, the aggressive expansion of WHT regimes—combined with the complexities of Zimbabwe’s multi-currency environment and tight filing deadlines under Statutory Instrument 81 of 2025—has created significant legal friction.

This article provides an exhaustive analysis of the twelve distinct WHT returns fileable on the TaRMS platform. It dissects their statutory triggers, calculation mechanics, judicial history, and practical compliance workflows.

2. Constitutional and Judicial Safeguards in Withholding Tax Administration

The collection of withholding tax often runs parallel to disputes over property rights and the separation of powers. Under Section 71 of the Constitution of Zimbabwe (2013), every person has the right to private property, and arbitrary deprivation of property by the state is unconstitutional. Because withholding taxes require the immediate transfer of funds to ZIMRA before a final tax liability is formally assessed, the drafting of these statutes must balance administrative efficiency with constitutional fairness.

A. The Principle of Arbitrary Deprivation: Law Society of Zimbabwe v Minister of Finance (99-SC-092)

The landmark Supreme Court ruling in Law Society of Zimbabwe and Mollat P.M. v Minister of Finance with AG intervening (99-SC-092) established the primary constitutional boundaries for withholding taxes. Under the old Section 36 of the Finance Act 29 of 1998, the legislature had introduced an aggressive withholding tax on property sales without providing a rapid refund mechanism for transactions where no actual capital gains were realized.

The Supreme Court held that forcing a taxpayer to suffer an arbitrary withholding tax without an immediate avenue to prove that no tax was due, or to secure a prompt refund, constituted an arbitrary deprivation of property, making the provision ultra vires Section 16 of the old Constitution. The court emphasized that while the state has a legitimate interest in collecting revenue, it cannot use collection mechanisms that act as permanent, non-consensual expropriations of wealth under the guise of “withholding.”

This ruling forced ZIMRA to restructure its capital gains withholding tax clearance system. It introduced Section 22C(5) of the Capital Gains Tax Act, which permits taxpayers to apply for a “clearance certificate” before the withholding agent (the depositary) remits the funds. This mechanism allows the taxpayer to prove that no capital gains tax is likely to be payable, or that the actual tax liability is less than the provisional withholding amount, thereby satisfying the constitutional requirement for administrative justice.

B. The Delegate Legislation Crisis: Gonese v Minister of Finance (22-HH-265)

Another major friction point in Zimbabwean tax law is the use of Statutory Instruments (SIs) to amend tax rates. Under Section 3 of the Finance Act [Chapter 23:04], the Minister responsible for finance is empowered to make regulations that amend or replace tax rates, duties, or levies, subject to future confirmation by an Act of Parliament within a specified timeframe.

In Gonese v Minister of Finance and Economic Development (22-HH-265) and M. Mlilo v Minister of Finance (19-HH-605), the High Court challenged this delegation of power. The court held that the executive branch, represented by the Minister of Finance, cannot unilaterally create or amend tax laws through regulations, as the power to levy taxes is a non-delegable prerogative of Parliament. While Parliament has repeatedly passed retrospective “validation” clauses to overrule these judgments, the tension between executive-driven tax changes and parliamentary oversight remains a major source of uncertainty for withholding agents.

3. Exhaustive Analysis of the Twelve Withholding Tax Returns

+-----------------------------------------------------------------------------------------------------------------+

| THE TWELVE WITHHOLDING TAX REGIMES IN ZIMBABWE |

+---------------------------------------------------------------------+-------------------------------------------+

| Return / Tax Type | Primary Governing Statute |

+---------------------------------------------------------------------+-------------------------------------------+

| 1. CGT WHT - Immovable Property and Intangibles | Part IIIA, CGT Act; Sec 39(b), Finance Act|

| 2. CGT WHT - Marketable Securities | Part IIIA, CGT Act; Sec 39(a), Finance Act|

| 3. Automated Financial Transaction Tax (AFTT) | Sec 36B, Taxes Act; Sec 22B, Finance Act |

| 4. Demutualisation Levy | Sec 36D, Taxes Act; Sec 22D, Finance Act |

| 5. Non-Resident WHT - Fees, Remittances, and Royalties | Sec 30-32, Taxes Act; Sec 19-21, Fin Act |

| 6. WHT on Non-Executive Directors’ Fees | Sec 36J, Taxes Act; Sec 22J, Finance Act |

| 7. WHT on Non-Resident Artistes and Entertainers | 17th/19th Schedule, Taxes Act |

| 8. Property or Insurance Commission Tax | Sec 36I, Taxes Act; Sec 22I, Finance Act |

| 9. Residents’ Tax on Interest | Sec 34, Taxes Act; Sec 22, Finance Act |

| 10. Shareholders’ Tax (Listed and Unlisted Dividends) | Sec 26 & 28, Taxes Act; Sec 15 & 17, Fin |

| 11. Withholding Tax on Tenders (Withholding on Contracts) | Sec 80, Taxes Act |

| 12. Withholding Tax on Gross Winnings of Betting Punters | Sec 36L, Taxes Act; Sec 22M, Finance Act |

+---------------------------------------------------------------------+-------------------------------------------+

Return 1: Capital Gains Withholding Tax – Immovable Property and Intangibles

A. Statutory Base and Charging Sections

Capital gains withholding tax on the transfer of immovable property and registered intangible rights is governed by Part IIIA of the Capital Gains Tax Act [Chapter 23:01], specifically Sections 22A, 22C, and 30A, read together with Section 39(b) of the Finance Act [Chapter 23:04].

Under Section 2(1) of the Capital Gains Tax Act, immovable property is defined as any land or buildings. Intangibles include registered rights to patents, trade marks, industrial designs, and copyright, as expanded by Finance Act 2 of 2017.

B. The Withholding Agent and Trigger Events

The obligation to withhold arises upon the “sale” or “deemed sale” (disposal otherwise than by sale under Section 8(2)(b)) of the specified asset. The withholding agent is defined under Section 22A as the “depositary.” A depositary includes:

- conveyancers and legal practitioners;

- registered estate agents holding the transaction funds;

- the Sheriff or Master of the High Court;

- local authorities or land developers mediating a cession of rights in a stand.

When a transaction is concluded, the depositary is legally mandated to withhold the tax from the purchase price and pay it to ZIMRA.

C. Applicable Rates and Calculations

Pursuant to Section 39(b) of the Finance Act:

- Assets Acquired After 22nd February 2019: The withholding rate is 15% of the gross sale proceeds. This acts as a provisional tax. The seller remains liable to file a final Capital Gains Tax return (Form CGT 1) within 15 days of the sale under SI 81 of 2025, where the final liability is assessed at 20% of the net capital gain (using the 2.5% straight-line deduction per annum under Section 39A(9a) for foreign currency transactions, or indexation for local currency transactions).

- Assets Acquired Before 22nd February 2019: The rate is 5% of the gross sale proceeds. This withholding is treated as a final tax on the transaction, preventing the complex, inflationary recalculation of historical pre-2019 assets.

D. Compliance, Clearance, and Judicial Precedents

Under Section 30A and Section 32, the Registrar of Deeds is prohibited from executing or registering any transfer of immovable property unless a Capital Gains Tax Clearance Certificate is produced.

In Sabeta M v Commissioner General: ZIMRA (12-HH-079), the High Court held that once a taxpayer has paid the calculated capital gains tax or withholding tax, ZIMRA cannot arbitrarily delay or refuse to issue the clearance certificate. The court emphasized that the issuance of the certificate is an administrative duty that must be performed expeditiously once the statutory financial obligations are met.

In Rouse S v ZIMRA (25-HH-315), the court evaluated the timing of the withholding trigger. The taxpayer argued that no tax could accrue until formal deeds registration occurred. The High Court rejected this, clarifying that under Section 18(1) and the definition of gross capital amount in Section 8(1)(a), the tax accrues on the date the binding agreement of sale is signed, not when title passes at the Deeds Registry. Therefore, the depositary must calculate and withhold the tax within 3 working days of receiving the transaction funds, as required by Section 22C(1).

Return 2: Capital Gains Withholding Tax – Marketable Securities

A. Statutory Base and Charging Sections

The withholding tax on the disposal of marketable securities is governed by Part IIIA of the Capital Gains Tax Act, read with Section 39(a) and 39(d) of the Finance Act. Marketable securities are defined under Section 2(1) as any bond capable of being sold in a share market, debentures, shares, or units in a registered unit trust scheme.

B. The Withholding Agent and Trigger Events

The trigger event is the disposal of the marketable security. The withholding agent under Section 22A is the “depositary” mediating the transaction, which is typically a registered stockbroker, financial institution, asset manager, or company secretary responsible for maintaining the share register.

C. Applicable Rates and Calculations

Under the Finance Act, the rates are categorized based on whether the security is listed or unlisted:

- Listed Marketable Securities (Section 39(a)): The withholding tax rate is 1% of the gross sale price. Pursuant to Section 39(a), this 1% withholding acts as a final tax. However, under Section 38(a)(iii), if a listed security is held for less than 180 days on the date of sale, the seller is subject to an additional tax rate of 4% of the capital gain, which is assessed during annual returns.

- Unlisted Marketable Securities (Section 39(d)): The rate is 5% of the gross sale price. Unlike listed securities, this withholding is provisional. The transaction must be reported via TaRMS, and a final Capital Gains Tax return must be submitted to assess the final 20% tax on the net capital gain.

D. Compliance and Judicial Precedents

Company secretaries are prohibited under Section 30A from registering the transfer of any unlisted corporate shares unless a digital ZIMRA tax clearance certificate is provided.

In Old Mutual Zimbabwe Ltd v Commissioner-General of ZIMRA (16-HH-143), the High Court examined a transaction where shares were sold from an Indigenisation Employee Share Trust to satisfy employees’ Pay As You Earn (PAYE) obligations. The taxpayer argued that this was an internal compliance transfer that should be exempt from capital gains tax. The court rejected this argument, ruling that the disposal of shares to raise cash for tax payments constitutes a taxable transaction under the Capital Gains Tax Act, thereby triggering the obligation to withhold and remit the tax.

Conversely, in Padenga Holding Ltd & 2 Ors v ZIMRA (25-HH-598), the High Court addressed internal corporate restructures. The court held that where shares are swapped between companies under the same control in the course of a merger, reconstruction, or group reorganisation, the companies can elect for roll-over relief under Section 15(1)(b). If this election is made, the transaction is deemed to have occurred at a price equal to the allowable deductions, resulting in a zero capital gain and exempting the transaction from immediate withholding tax.

Return 3: Withholding Tax on Automated Financial Transaction Tax (AFTT)

A. Statutory Base and Charging Sections

The Automated Financial Transaction Tax (AFTT) is a specialized tax levied under Section 36B of the Income Tax Act, with the rate fixed by Section 22B of the Finance Act. This tax represents Zimbabwe’s fiscal response to the rise of electronic banking and automatic teller machine (ATM) transactions, designed to capture revenue from automated cash movements.

B. The Withholding Agent and Trigger Events

The tax is triggered whenever a customer executes a cash withdrawal through an ATM, point-of-sale machine, or any other automated device operated by a banking institution. The withholding agent is the financial institution or commercial bank executing the electronic withdrawal. The bank must automatically deduct the tax from the customer’s account balance during the transaction.

C. Applicable Rates and Calculations

Following amendments in the Finance Act 2024 and SI 80 of 2024, the rates for AFTT are:

- Local Currency (ZiG) Withdrawals: For each withdrawal above the local currency equivalent of USD 100, the tax is the local currency equivalent of USD 0.05.

- Foreign Currency (USD) Withdrawals of USD 1,000 or Less: A flat tax of USD 0.05 per transaction.

- Foreign Currency (USD) Withdrawals Above USD 1,000: The tax is 1% of the total value of the withdrawal.

D. TaRMS Administration and Compliance

The bank is required to compile all daily AFTT deductions and file a monthly return on the TaRMS portal. Unlike other standard income tax heads, AFTT does not allow for any deductions or tax credits. It is a transactional levy that must be remitted by the withholding bank using the SBA platform, with strict currency separation enforced (ZiG and USD transactions are posted to separate sub-accounts).

Return 4: Withholding Tax on Demutualisation Levy

A. Statutory Base and Charging Sections

The Demutualisation Levy is charged under Section 36D of the Income Tax Act, read with Section 22D of the Finance Act and the Twenty-Seventh Schedule to the Taxes Act.

B. Trigger Events and historical Application

The levy was introduced to target the massive windfall of wealth created during the demutualisation of mutual societies—such as Old Mutual and First Mutual—when they transitioned from policyholder-owned mutual societies into corporate entities listed on public stock exchanges. The levy is triggered when a mutual society distributes “windfall shares” or cash portions to its newly registered corporate members and individual policyholders in Zimbabwe.

C. Applicable Rates and Calculations

Under Section 22D of the Finance Act, the levy is calculated at a flat rate of 2.5% of the value of the shares issued or the cash distributed to each Zimbabwean member of the mutual society. The mutual society itself acts as the withholding agent. It is legally mandated to withhold 2.5% of the total share volume or cash allocation before distributing the balance to the beneficiaries.

D. TaRMS Compliance and Modern Relevance

While demutualisation events are rare in the modern corporate landscape, the return remains a statutory fixture on the TaRMS portal. Any corporation or insurance entity seeking to undergo a demutualisation restructure must activate this return, perform the calculations based on the fair market value of the underlying assets on the date of listing, and remit the levy in the currency of the transaction.

Return 5: Withholding Tax on Fees, Remittances, and Royalties (Non-Resident)

A. Statutory Base and Charging Sections

This return consolidates three critical non-resident withholding taxes designed to prevent the extraction of untaxed wealth from Zimbabwe through cross-border payments:

- Non-Residents’ Tax on Fees: Section 30 of the Taxes Act, Section 19 of the Finance Act, and the Seventeenth Schedule.

- Non-Residents’ Tax on Remittances: Section 31 of the Taxes Act, Section 20 of the Finance Act, and the Eighteenth Schedule.

- Non-Residents’ Tax on Royalties: Section 32 of the Taxes Act, Section 21 of the Finance Act, and the Nineteenth Schedule.

B. Trigger Events and Definitions

- Fees: Triggered by payments made to non-resident persons or foreign corporations for technical, managerial, administrative, or consulting services performed within or outside Zimbabwe, provided the source of the payment is Zimbabwean.

- Remittances: Triggered when a local subsidiary or branch remits funds to its foreign parent company or head office to cover allocable administrative or head office expenses.

- Royalties: Triggered by payments made to non-residents for the use of, or the right to use, intellectual property, including patents, designs, trade marks, copyright, secret formulas, and industrial or scientific equipment.

C. Applicable Rates and Calculations

Under the Finance Act, the tax is calculated as a flat percentage of the gross amount payable:

- Non-Residents’ Tax on Fees: 15% of each dollar paid.

- Non-Residents’ Tax on Remittances: 15% of each dollar remitted.

- Non-Residents’ Tax on Royalties: 15% of each dollar paid.

No deductions or business expenses can be claimed against these taxes. They are calculated on the gross value of the invoice or remittance transaction.

D. Currency of Payment, Double Taxation Agreements, and Case Law

Under Section 4A(1)(c), if the underlying contract is denominated in foreign currency, the withholding tax must be remitted in foreign currency (specifically United States Dollars).

In Delta Corporation Limited v ZIMRA (24-SC-062), the Supreme Court examined the application of withholding taxes in multi-currency transactions. The court held that where a taxpayer trades in foreign currency, they must account for and pay tax in the same foreign currency. Delta had attempted to pay taxes in local currency using historical rates of exchange. The Supreme Court confirmed that the state is entitled to receive the tax in the exact currency that was used to conclude the underlying transaction.

In Unki Mines (Pvt) Ltd v ZIMRA and Stanbic Bank (22-HH-729), the High Court addressed the issue of ZIMRA using “agency appointments” (appointing commercial banks to freeze taxpayer funds) to collect disputed withholding taxes on foreign service fees. The court held that while ZIMRA has the statutory power to appoint agents under Section 58 of the Taxes Act, it must strictly adhere to administrative justice principles, and cannot execute arbitrary attachments before an objection has been formally evaluated.

Furthermore, these non-resident withholding taxes are subject to relief under Double Taxation Agreements (DTAs). If the non-resident is resident in a country that has a DTA with Zimbabwe (such as South Africa, the United Kingdom, or China), the withholding tax rates may be capped at lower rates (typically 10% or 5%), provided the non-resident submits a valid Tax Residency Certificate to ZIMRA prior to the payment.

Return 6: Withholding Tax on Non-Executive Directors’ Fees

A. Statutory Base and Charging Sections

Withholding tax on non-executive directors’ fees is governed by Section 36J of the Taxes Act, Section 22J of the Finance Act, and the Thirty-Third Schedule to the Taxes Act. This tax was introduced to eliminate tax evasion among high-earning corporate directors who previously classified their income as non-employment board fees to avoid progressive PAYE brackets.

B. The Withholding Agent and Trigger Events

The trigger event is the payment of any director’s fees, allowances, or other remuneration to a non-executive director of a company, whether the director is resident or non-resident in Zimbabwe. The withholding agent is the paying company.

C. Applicable Rates and Calculations

Under Section 22J of the Finance Act, the tax is calculated at a flat rate of 20% of each dollar of the fee or allowance paid. Unlike executive directors who are subject to PAYE progressive tax tables (up to 40%), non-executive directors are taxed at this flat 20% rate.

D. final Tax Status and TaRMS Workflow

Under the Thirty-Third Schedule, this withholding tax is a final tax. The non-executive director does not need to declare this income in their annual personal income tax returns, nor can they claim any business deductions against it. The company must file the return on TaRMS by the 5th day of the month following the payment under SI 81 of 2025, and pay the tax in the currency of the transaction.

Return 7: Withholding Tax on Non-Resident Artistes and Entertainers

A. Statutory Base and Charging Sections

This withholding tax is administered under the general non-resident fees framework of the Taxes Act, read with the Seventeenth and Nineteenth Schedules. It targets foreign musicians, actors, sports teams, public speakers, and other entertainers who perform short-term shows or commercial activities in Zimbabwe.

B. The Withholding Agent and Trigger Events

The trigger event is the payment of performance fees, booking fees, or promotional fees to a non-resident entertainer or their agent for services rendered in Zimbabwe. The withholding agent is the local promoter, event organizer, or corporate sponsor hosting the foreign artist.

C. Applicable Rates and Calculations

The tax is calculated at a flat rate of 15% of the gross fees payable to the artist. If the foreign artist receives their payment in foreign currency (as is standard in international entertainment contracts), the local promoter must withhold 15% of the contract value in foreign currency and remit it via TaRMS.

D. Compliance and Clearance

To enforce compliance, ZIMRA collaborates with the National Arts Council of Zimbabwe and the Department of Immigration. Foreign artists are generally denied temporary employment permits or performance clearance unless the local promoter can produce a ZIMRA withholding tax clearance certificate or prove that the 15% tax has been withheld and paid.

Return 8: Withholding Tax on Property or Insurance Commission Tax

A. Statutory Base and Charging Sections

Property or Insurance Commission Tax is levied under Section 36I of the Taxes Act, Section 22I of the Finance Act, and the Thirty-Second Schedule to the Taxes Act.

B. Trigger Events and the Role of Withholding Agents

The tax is triggered when an insurance company or a real estate entity pays a commission or brokerage fee to an independent insurance agent, broker, or freelance estate agent. The withholding agent is the paying insurance house or property development company.

C. Applicable Rates and Calculations

Under Section 22I of the Finance Act, the tax is calculated at a flat rate of 20% of each dollar of the commission paid. This regime was established to bring freelance commission earners—who often operate in the informal market without registering for income tax—into the tax net.

D. TaRMS Compliance and final Tax Status

The 20% withholding tax acts as a final tax for independent, non-corporate commission agents. The withholding agent must compile all monthly commissions, declare them on the designated TaRMS return by the 5th day of the following month, and allocate the payments in the corresponding ZiG or USD ledgers.

Return 9: Withholding Tax on Residents’ Tax on Interest

A. Statutory Base and Charging Sections

Residents’ Tax on Interest is governed by Section 34 of the Taxes Act, Section 22 of the Finance Act, and the Twenty-First Schedule to the Taxes Act. It applies to interest earned by residents of Zimbabwe on deposits with financial institutions.

B. The Withholding Agent and Trigger Events

The tax is triggered whenever a financial institution (commercial bank, building society, or discount house) pays or credits interest to a resident depositor’s account. The bank itself acts as the withholding agent.

C. Applicable Rates and Calculations

Under Section 22 of the Finance Act, the rates are split based on the tenure of the deposit:

- Fixed-Term Deposits with a Tenure of 90 Days or More: The withholding tax rate is 5% of each dollar of interest earned. This lower rate is designed to encourage long-term savings in the formal banking sector.

- Other Accounts (Savings Accounts, Demand Deposits, and Call Accounts): The rate is 15% of each dollar of interest earned.

D. Exemptions and Compliance

The Twenty-First Schedule provides exemptions for interest earned by the state, local authorities, statutory bodies, and pension funds. Under the TaRMS portal, banks must file a monthly residents’ tax on interest return, dividing the interest paid and tax withheld between ZiG and USD accounts.

Return 10: Withholding Tax on Shareholders’ Tax – Listed and Unlisted Dividends

A. Statutory Base and Charging Sections

The taxation of dividends distributed by Zimbabwean companies is split into two frameworks:

- Resident Shareholders’ Tax: Section 28 of the Taxes Act, Section 17 of the Finance Act, and the Fifteenth Schedule.

- Non-Resident Shareholders’ Tax: Section 26 of the Taxes Act, Section 15 of the Finance Act, and the Ninth Schedule.

B. The Withholding Agent and Trigger Events

The tax is triggered by the distribution of dividends by any company registered or incorporated under the Companies and Other Business Entities Act [Chapter 24:31]. The withholding agent is the company declaring and distributing the dividend.

C. Applicable Rates and Calculations

- Resident Shareholders’ Tax (Section 17):

- Listed Securities: If the dividend is distributed from a security listed on a registered securities exchange (such as the Zimbabwe Stock Exchange), the rate is 10%.

- Unlisted Securities: For private companies, the rate is 15% of the gross dividend.

- Non-Resident Shareholders’ Tax (Section 15):

- Listed Securities (ZSE): Capped at 10%.

- Victoria Falls Stock Exchange (VFEX): Dividends distributed from VFEX-listed companies enjoy a concessionary rate of 5%.

- Unlisted Securities: Capped at 15%.

D. final Tax Status and TaRMS Workflow

Withholding on dividends is a final tax in Zimbabwe. Under the Fifteenth and Ninth Schedules, the company must file the return on TaRMS within the statutory deadline (by the 5th day of the following month under SI 81 of 2025) and pay ZIMRA in the currency of the dividend distribution.

Return 11: Withholding Tax on Tenders (Withholding on Contracts)

A. Statutory Base and Charging Sections

Withholding Tax on Contracts—commonly referred to as Withholding Tax on Tenders—is governed by Section 80 of the Income Tax Act. It is one of ZIMRA’s most effective administrative tools for policing the informal sector and ensuring corporate compliance.

B. Trigger Events and the Obligation to Withhold

The tax is triggered when a registered corporate taxpayer, statutory body, or state agency makes a payment to a supplier or contractor for goods, services, or construction works under a contract, where the aggregate value of the transactions exceeds the statutory threshold during a tax year.

The obligation to withhold arises if the supplier cannot produce a valid Tax Clearance Certificate (ITF263) at the time of the payment. The paying company must act as the withholding agent and deduct the tax at source.

C. Applicable Rates and Calculations

Following amendments in recent Finance Acts, the withholding rate on contracts is a flat 30% of the gross contract value. This is a significant increase from the historical 10% rate, making it a severe financial penalty for non-compliant suppliers.

D. Compliance, the ITF263 System, and TaRMS portal Integration

If the supplier has a valid digital ITF263, the withholding agent pays the full invoice amount. If the supplier does not have it, the agent must withhold 30%, pay the remaining 70% to the supplier, and file a return (Form REV 5) on TaRMS to remit the 30% portion. ZIMRA then credits this 30% payment to the supplier’s income tax ledger. The supplier can claim this as a tax credit when they file their annual corporate self-assessment return (Form ITF 12C).

Return 12: Withholding Tax on Gross Winnings of Betting Punters

A. Statutory Base and Charging Sections

The taxation of betting and gaming in Zimbabwe is governed by Section 36L of the Taxes Act, read with Section 22M of the Finance Act and the Thirty-Sixth Schedule to the Taxes Act, as substituted by Finance Act 7 of 2025 (effective 1st January 2026).

B. The Withholding Agent and Trigger Events

The tax is triggered when a punter (customer) wins a bet or a payout from a licensed gaming operator, casino, or betting promoter. The withholding agent is the licensed gaming or betting operator.

C. Applicable Rates and Calculations

Under Section 22M of the Finance Act:

- Gaming Operators Tax: The operator pays a tax of 20% of their gross monthly takings.

- Punters Tax: The operator must withhold 25% of the gross winnings of the punters before distributing the balance.

D. TaRMS Administration and Compliance

The gaming operator must keep detailed records of all individual payouts, compile the daily punters’ tax deductions, and file the monthly return on the TaRMS portal. The fiscus enforces strict multi-currency calculations under Section 4A, meaning that if a punter places a bet and wins in USD, the 25% withholding tax must be remitted to ZIMRA in USD.

4. Currency Dynamics and the Section 4A Multi-Currency Framework

Accounting for and paying taxes in Zimbabwe is complicated by the dual-currency monetary system, which currently features both the local currency (Zimbabwe Gold – ZiG) and the United States Dollar (USD). The fiscus monitors this through the strict application of Section 4A of the Finance Act [Chapter 23:04].

+--------------------------------------------+

| SECTION 4A CURRENCY COMPLIANCE PATH |

+---------------------+----------------------+

|

Does the withholding agent receive or pay

funds in a specified foreign currency (USD)?

|

+----------------------+----------------------+

| |

YES NO

| |

Withhold tax in USD. Withhold tax in ZiG.

Remit to USD sub-account Remit to ZiG sub-account

on TaRMS portal. on TaRMS portal.

| |

+----------------------+----------------------+

|

[ SUBMIT RETURN ON TaRMS ]

A. The “Currency of Transaction” Rule

Section 4A establishes the fundamental rule that tax must be paid in the same currency as the underlying transaction. If a company pays a dividend in USD, the Shareholders’ Tax must be withheld and paid in USD. If technical fees are invoiced in USD, the Non-Residents’ Tax on Fees must be remitted in USD. Under Section 4A(9), it is statutory-presumed that every transaction was conducted using the United States Dollar only, unless the taxpayer can produce documentary proof (such as an invoice or bank statement) showing that the transaction was conducted in local currency.

B. The 50% Rule and its Practical Implications

Effective 1st July 2024, a major amendment to Section 4A was introduced. Where any company, partnership, or trust receives or accrues more than 50% of its total income in foreign currency, that entity is deemed to have earned half of its income in foreign currency and the other half in local currency.

Consequently, the entity must account for and pay its taxes—including provisional taxes (QPDs)—on a 50/50 basis. For the portion of the tax that must be converted from USD to ZiG, the payment must be made using the official interbank rate on the day of payment.

C. Analysis of Judicial Precedents on Multi-Currency Compliance

In Zimplats v ZIMRA (22-HH-845), the High Court addressed the conflict between exchange control regulations and tax laws. Zimplats had argued that because it was forced to liquidate a portion of its foreign currency earnings into local currency under the Reserve Bank of Zimbabwe (RBZ) mandatory retention schemes, it should be permitted to pay its taxes on that liquidated portion in local currency.

The High Court confirmed that under Section 4A(10), any income that is liquidated and paid in local currency upon transfer to a nostro account is calculated as if it was earned in local currency, allowing the taxpayer to pay that portion of the tax in local currency (ZiG).

However, in Redan Petroleum (Pvt) Ltd v ZIMRA (23-HH-637), the court rejected Redan’s attempt to settle historical foreign currency tax liabilities in local currency. The court emphasized that the Commissioner-General has no discretion to accept local currency for taxes that are legally due in foreign currency under Section 4A, and any attempt to do so violates the principle of legality.

In Contitouch Technologies (Pvt) Ltd v ZIMRA and CBZ Bank (25-HH-057), the High Court further clarified that commercial banks, when acting as agent collectors for ZIMRA, must freeze and remit funds in the specific currency demanded by ZIMRA’s agency appointment notice. If ZIMRA issues an agency notice in USD, the bank cannot satisfy that debt by transferring local currency (ZiG) balances unless ZIMRA explicitly amends the notice.

5. TaRMS Administration, Penalties, and Dispute Resolution

The Tax Revenue Management System (TaRMS) has centralized tax compliance in Zimbabwe. Under this system, all tax heads are linked to a single Taxpayer Identification Number (TIN) and managed through the Single Business Account (SBA).

A. Automatic Penalty Calculations

The TaRMS portal features automated calculations of late-filing and late-payment penalties, removing the previous administrative discretion of ZIMRA officers.

Under Section 22H of the Capital Gains Tax Act and general provisions of the Taxes Act, failing to submit a return or remit withholding tax by its statutory due date triggers an automatic civil penalty. This penalty consists of:

- The Tax Due: The primary tax liability is posted to the SBA ledger.

- Late Payment Penalty: A flat civil penalty of 15% of the unpaid withholding tax is automatically applied.

- Interest: Late-payment interest is calculated daily in terms of Section 26(3) at rates fixed by the Minister by statutory instrument (as set out in SI 211 of 2022).

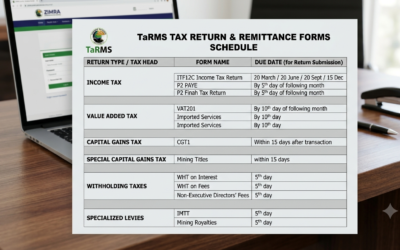

B. The Separated Due Dates (SI 81 of 2025)

Under Statutory Instrument 81 of 2025, the fiscus introduced a critical structural change: the separation of the due date for submitting tax returns from the due date for tax payments. Returns must now be filed earlier to allow the TaRMS ledger to validate the liability, while payments remain payable on their traditional statutory payment due dates.

- Capital Gains Withholding Tax (Immovable Property and Marketable Securities): Return submission is due within 15 days from the transaction date, rather than the historical 30-day window.

- Residents’ Tax on Interest and Shareholders’ Tax: Return submission is due by the 5th day of the following month, while payment is due by the 10th.

- VAT Withholding Tax: Return submission is due by the 10th day of the following month, while payment is due by the 25th.

C. The Dispute Resolution Process: Section 62 and 63 of the Taxes Act

If a withholding agent or a taxpayer disputes an assessment, a valuation adjustment under Section 14, or an automatic penalty, they must follow the statutory dispute resolution process set out in Part VI of the Capital Gains Tax Act and Sections 62 to 70 of the Taxes Act.

- Lodging an Objection: Under Section 25(1) of the CGT Act and Section 62 of the Taxes Act, the taxpayer must file a written objection on the TaRMS portal within 30 days of receiving the assessment or decision. The objection must outline the specific grounds of dispute.

- The “Pay Now, Argue Later” Principle: Under general Zimbabwean tax law, lodging an objection does not suspend the obligation to pay the assessed tax unless the Commissioner-General grants an explicit extension under Section 26(3). This means that ZIMRA can continue to enforce collection through bank agency appointments even while the dispute is being reviewed.

- Appeals: If the objection is disallowed by the Commissioner-General, the taxpayer has the right to appeal to the Fiscal Appeal Court or the High Court within 30 days under Section 25(2), read with Sections 63 to 70 of the Taxes Act.

6. Conclusion and Strategic Best Practices for Withholding Agents

The rapid expansion of withholding tax regimes in Zimbabwe has shifted the administrative burden of tax collection onto the private sector. With the implementation of the TaRMS portal and the tight timelines under SI 81 of 2025, withholding agents must maintain highly disciplined accounting records.

To ensure compliance and protect themselves from automatic penalties and ZIMRA audits, businesses in Zimbabwe should adopt several best practices:

- Automate Multi-Currency Ledger Splits: Ensure that your ERP and accounting systems can track and separate transactions in ZiG and USD on an invoice-by-invoice basis, matching the requirements of Section 4A.

- Implement Real-Time Tax Clearance Checks: Before paying any supplier, corporate buyers must check ZIMRA’s portal to verify if the supplier has a valid digital ITF263 tax clearance certificate. If they do not, the 30% withholding tax on contracts must be deducted immediately.

- Engage with Double Taxation Agreements (DTAs): When dealing with foreign suppliers, non-executive directors, or investors, always verify if they qualify for DTA relief. Secure their Tax Residency Certificates before applying the standard 15% non-resident withholding rates.

- Monitor the Single Business Account (SBA) Ledger: Regularly check your SBA dashboard on the TaRMS portal to identify any unallocated credits, pending returns, or automatic penalty postings, ensuring that errors are contested within the statutory 30-day objection window.

By combining strict administrative compliance with a deep understanding of statutory exemptions and judicial precedents, corporate withholding agents can navigate the complexities of Zimbabwe’s fiscal landscape while maintaining operational efficiency.