Tax and Regulatory Implications of Shareholder Loans in the Form of Equipment: A Case Study of Chinese Investment in Zimbabwe

When a Chinese shareholder provides equipment to a Zimbabwean company as a loan (a “loan-in-kind”), the transaction triggers a complex cascade of tax and regulatory obligations. This comprehensive analysis examines the Zimbabwean tax framework, focusing on Corporate Income Tax, Thin Capitalization rules, Withholding Taxes (WHT), Value Added Tax (VAT), and the relief provided by the Zimbabwe-China Double Taxation Agreement (DTA). In an era of heightened ZIMRA (Zimbabwe Revenue Authority) scrutiny, understanding the intersection of the Income Tax Act [Chapter 23:06] and international treaties is essential for protecting foreign direct investment (FDI).

The Mechanics of “Credit for Assets”

In the context of China-Zimbabwe economic cooperation, it is common for a parent company or major shareholder in China to provide “capital equipment” (machinery, specialized tools, or technical infrastructure) to its Zimbabwean subsidiary on credit. Legally, this is not an equity injection but a debt obligation.

The Zimbabwean company (the debtor) acquires the equipment and recognizes a liability to the Chinese shareholder (the creditor). Because the principal of this loan is an asset rather than cash, it is often termed a “loan-in-kind.” For tax purposes, this creates three distinct areas of concern:

- Valuation: What is the “cost” of the asset for tax purposes?

- Deductibility: Is the interest paid on this equipment loan tax-deductible?

- Remittability: Can the Zimbabwean company legally pay back the loan in foreign currency?

The primary legislative pillars governing this are:

- The Income Tax Act [Chapter 23:06] (The bedrock of corporate and withholding tax)

- The Value Added Tax Act [Chapter 23:12] (Governing import VAT)

- The Finance Act [Chapter 23:04] (Specifying tax rates and AIDS levies)

- The Exchange Control Act [Chapter 22:05] (Governing foreign debt registration)

- Statutory Instrument 114 of 2016 (The Zimbabwe-China Double Taxation Agreement)

Income Tax Implications for the Zimbabwean Entity

Capital Allowances and the Fourth Schedule

Under the Fourth Schedule of the Income Tax Act, the Zimbabwean company is the owner of the equipment for tax purposes (assuming the risks and rewards of ownership have passed). This allows the company to claim capital allowances, which are essential for reducing taxable income.

- Special Initial Allowance (SIA): Per Paragraph 9 of the Fourth Schedule, a taxpayer may claim an SIA of 25% of the cost of the equipment in the year it is first used and in each of the subsequent three years. This is applicable if the equipment is used for industrial, agricultural, or mining purposes.

- Wear and Tear: If the company opts not to use SIA, it may claim a wear and tear allowance (depreciation) at rates typically ranging from 10% to 20% per annum, depending on the nature of the machinery.

The Valuation Challenge:

Section 23 of the Income Tax Act grants the Commissioner-General of ZIMRA the power to adjust the “purchase price” of any property if it is not at “arm’s length.” If the Chinese investor provides equipment valued at $1,000,000 that has a market value of $600,000, ZIMRA will:

- Reduce the basis for capital allowances to $600,000.

- Disallow the interest expense related to the inflated $400,000 portion.

Thin Capitalization and the 3:1 Ratio

Zimbabwean tax law is highly protective against “profit stripping” a practice where a company uses excessive debt to move profits out of the country via interest payments.

Section 16(1)(q) of the Income Tax Act dictates that:

No deduction shall be made in respect of any expenditure or loss to the extent to which it is interest on that portion of the debt which causes the debt-to-equity ratio to exceed 3:1.

Application:

If the Zimbabwean company has an equity (share capital + reserves) of $100,000 and the equipment loan is $500,000, the total debt exceeds the 3:1 threshold ($300,000). The interest on the “excess” $200,000 of the loan will be disallowed as a deduction for corporate tax.

The “Deemed Dividend” Consequence

Perhaps the most overlooked implication is that disallowed interest is not just “lost” as a deduction. Under the Finance Act, any interest disallowed under the thin capitalization rules is re-characterized as a dividend.

- This triggers Non-Resident Shareholders’ Tax (NRST).

- Normally, NRST is 15%.

- This creates a double-taxation trap: the company pays corporate tax on the disallowed interest (as it’s not deducted), AND the shareholder pays withholding tax on that same amount as a “deemed dividend.”

Taxation of the Chinese Investor (The Creditor)

Withholding Tax on Interest (Section 34)

In a standard cross-border loan, the Zimbabwean borrower must withhold tax from any interest paid to the non-resident lender.

- Domestic Rate: 15% under Section 34 of the Income Tax Act.

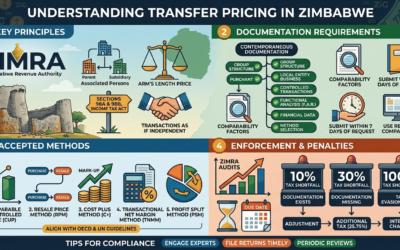

- DTA Relief: The Zimbabwe-China Double Taxation Agreement (S.I. 114 of 2016) provides significant relief. Under Article 11, the withholding tax on interest is capped at 7.5%, provided the recipient is the “beneficial owner.”

Compliance Requirement:

To access the 7.5% rate, the Chinese investor must provide a Tax Residency Certificate issued by the State Administration of Taxation (SAT) in China. Without this, ZIMRA will insist on the full 15%.

Transfer Pricing and “Arm’s Length” Interest

Under the Thirty-Fifth Schedule, Zimbabwe has adopted comprehensive Transfer Pricing (TP) guidelines based on the OECD model.

- The interest rate on the equipment loan must be “arm’s length.”

- If the Chinese shareholder charges 12% interest when a commercial bank would charge 6%, ZIMRA will disallow the 6% differential.

- The company is required to maintain a Transfer Pricing Policy Document annually to justify the rate.

Permanent Establishment (PE) Hazards

Article 5 of the DTA defines a Permanent Establishment. If the Chinese investor provides the equipment but also sends a team of engineers to Zimbabwe for more than 183 days in a 12-month period to maintain or operate that equipment, the investor may be deemed to have a “Service PE” in Zimbabwe.

- Consequence: The interest income and any service fees would be taxed at the full corporate rate (24% + 3% AIDS Levy) rather than the 7.5% withholding tax, as the income would be “effectively connected” to the Zimbabwean PE.

Value Added Tax (VAT) and Customs

Import VAT (Section 12 of the VAT Act)

When the equipment crosses the border, it is treated as a “taxable supply” of imported goods.

- Rate: 15%.

- Base: The Value for Duty Purposes (VDP) + any Customs Duty.

- Deferment: Under Section 12A, companies can apply to ZIMRA for a VAT Deferment on capital goods. This allows the company to import the equipment without paying the 15% VAT upfront, provided the equipment is used for manufacturing, mining, or agriculture. The VAT is effectively “pushed” to the next tax return, where it is often offset by input tax credits.

Customs Duty Rebates

Equipment for specific sectors often qualifies for rebates under the Customs and Excise (General) Regulations.

- Mining: Rebates are available for equipment used in prospecting or mining.

- Manufacturing: Rebates for capital equipment for “new projects.”

- ZIDA (Zimbabwe Investment and Development Agency) License: Holding a ZIDA license (under the ZIDA Act [Chapter 14:38]) is often a prerequisite for these high-level tax incentives.

Exchange Control and Regulatory Regularization

In Zimbabwe, a “loan-in-kind” is legally considered an external debt obligation.

RBZ Approval and Registration

Under the Exchange Control Act [Chapter 22:05] and S.I. 110 of 1996, all foreign loans must be registered with the Reserve Bank of Zimbabwe’s External Loans Coordinating Committee (ELCC).

- Registration Process: The company must submit the loan agreement and a “Form 21” (Bill of Entry) proving the equipment was imported.

- Risk of Non-Registration: If the loan is not registered, the Zimbabwean company will be prohibited from purchasing foreign currency to pay the interest or repay the principal. ZIMRA may also refuse to allow interest deductions for a loan that is not “regularized.”

Valuation Verification

The RBZ often cross-checks the value of imported equipment against global price databases to prevent “under-invoicing” or “over-invoicing” used for illicit financial flows. A third-party valuation certificate from an internationally recognized firm (e.g., SGS or Bureau Veritas) is highly recommended.

Relevant Case Law and ZIMRA Doctrines

While Zimbabwe has limited published tax litigation specifically on China-direct loans, the following principles from the Supreme Court and High Court are applied by ZIMRA auditors:

- Substance Over Form (ITC 1496): This regional doctrine, followed in Zimbabwe, allows ZIMRA to ignore the “label” of a transaction. If a “loan” has no repayment date, zero interest, or is subordinated to all other creditors, ZIMRA may argue it is equity in disguise. If re-characterized as equity:

- No interest is deductible.

- Any payments made to the shareholder are treated as dividends (subject to 15% NRST).

- Wholly and Exclusively (Commissioner of Taxes v. Astra Holdings): For interest to be deductible, the company must prove it was incurred for the purpose of trade. If the equipment is sitting idle or is not essential to the business, the interest deduction will be disallowed.

- The “Nostro” Account Precedent (G Bank Zimbabwe v. ZIMRA HH207-15): This case highlighted the importance of how offshore funds and loans are characterized and tracked. It serves as a warning that ZIMRA will closely monitor the “source” of funds and the “nexus” to Zimbabwean operations.

Comparative Analysis: Debt vs. Equity

| Feature | Shareholder Loan (Equipment) | Equity Investment (Equipment) |

| Tax Impact (Borrower) | Interest is deductible (up to 3:1 ratio). | Dividends are NOT deductible. |

| Tax Impact (Lender) | 7.5% WHT (under DTA). | 15% NRST (or 10% for listed cos). |

| Capital Allowances | Claimable by Borrower. | Claimable by Borrower. |

| Repayment | Contractual obligation; priority. | No fixed repayment; subordinate. |

| ZIMRA Scrutiny | High (Thin Cap & TP focus). | Moderate (Valuation focus). |

Strategic Recommendations for Investors

Pre-Investment Structuring

Investors should conduct a “Thin Capitalization Audit” before signing the loan agreement. If the loan-to-equity ratio is 10:1, the investor should consider converting a portion of the equipment value into Ordinary Shares (equity) to reach the 3:1 threshold, ensuring the remaining interest is fully deductible.

Documentation Checklist

A robust tax defense file should include:

- Signed Loan Agreement: Stating the principal, interest rate (referencing SOFR/Libor), and repayment schedule.

- Bill of Entry (Form 21): Stamped by ZIMRA Customs.

- Transfer Pricing Policy: Explicitly justifying the interest rate and equipment price.

- DTA Certificate of Residence: From the Chinese SAT.

- RBZ Approval Letter: Confirming the loan is registered and interest can be remitted.

ZIDA Utilization

Registering the investment with the Zimbabwe Investment and Development Agency (ZIDA) provides a layer of legal protection. Under the ZIDA Act, foreign investors are guaranteed against expropriation and are granted the right to transfer funds (profits, interest, and capital) “in a freely convertible currency without restriction.”

Conclusion

The provision of equipment as a shareholder loan is a double-edged sword in the Zimbabwean tax environment. While it offers a mechanism for tax-efficient profit repatriation through interest and capital allowances, it is governed by a rigid “3:1” thin capitalization rule and strict transfer pricing oversight.

For the Chinese investor, the Zimbabwe-China DTA is the most powerful tool for tax optimization, halving the withholding tax on interest. However, this benefit is only accessible if the loan is correctly registered with the Reserve Bank of Zimbabwe and supported by “arm’s length” documentation. In the absence of such planning, the “deemed dividend” rule and the potential disallowance of capital allowances can transform a strategic investment into a significant fiscal liability.