The Ides of March : A Dive into MPC Resolutions (24 March 2026)

The Monetary Policy Committee (MPC) meeting of March 2026 arrives at a critical juncture for the Zimbabwe Gold (ZiG) currency. While the central bank has maintained a hawkish stance to curb inflation, the divergence between official narratives and market realities, specifically regarding exchange rate flexibility and money supply thus creates a complex landscape for investors and local industry.

Major Highlights & Policy Resolutions

1. Interest Rate Maintenance

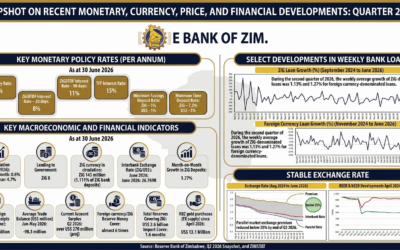

The MPC resolved to maintain the Bank Policy Rate at 35%.

- Analysis: This is a prudent “hold” that acknowledges persistent inflationary pressures. By keeping rates high, the RBZ aims to discourage speculative borrowing, though it simultaneously increases the cost of working capital for the formal sector.

2. Relief for Small-Scale Miners

The suspension of the proposed 10% surrender requirement for small-scale miners is a significant victory for the sector.

- Economic Impact: This move reverses a policy that was widely criticized as a “tax on production.” By allowing miners to retain more of their foreign currency earnings, the RBZ likely hopes to incentivize formal deliveries and boost the country’s actual gold reserves.

Critical Critique: The “Fixed” Exchange Rate Paradox

Despite the RBZ’s continued use of “willing-buyer, willing-seller” (WBWS) terminology, market data suggests the ZiG has become a fixed exchange rate in all but name.

- Global Disconnect: While international commodity markets and regional currencies have experienced significant volatility, the ZiG has remained strangely static.

- The Credibility Gap: For a currency to be credible, it must reflect market fundamentals. If the ZiG does not move when global markets shift, it suggests heavy-handed intervention rather than a market-determined rate. This creates a “pressure cooker” effect where the gap between the official and parallel rates is likely to widen.

The Treasury-Supplier Conflict

A glaring omission in the latest MPS is the silence regarding the Treasury’s move to pay suppliers in ZiG. This presents two major risks:

- Inflationary Liquidity: Paying large-scale contractors in local currency creates a sudden surge in ZiG liquidity. Without a deep and liquid functional market to convert this to USD, these suppliers naturally offload ZiG for hard currency to settle domestic costs.

- The Fuel Dilemma: Most domestic supply chain costs—most notably fuel—remain priced exclusively in USD. The MPS failed to provide a mechanism for how a company paid in ZiG is expected to purchase USD-denominated inputs without triggering a massive depreciation of the local unit.

Money Supply and the Inflation Narrative

The RBZ’s “single-digit inflation” narrative is increasingly at odds with its 37% annual money supply growth (as of December 2025).

- Supply-Side Shocks: The recent jump in crude oil prices is a classic supply-side shock. While monetary policy shouldn’t necessarily react to the shock itself, it must react to the accommodation of that shock through money creation.

- Inflation Expectations: High money growth acts as a precursor to future inflation (pass-through). Until the RBZ provides a credible roadmap for tapering this extraordinary growth, inflation expectations among businesses and citizens will remain stubbornly high.

Utilization of Foreign Exchange Reserves

A fundamental question remains regarding the utility of Zimbabwe’s foreign exchange reserves.

- The Buffer Argument: Foreign reserves exist specifically to cushion the economy against external shocks (like geopolitical tensions affecting oil).

- Policy Failure: Instead of using reserves to “smooth” the impact of fuel price increases, the authorities appear to be absorbing the shocks passively. Given that prices are “sticky downwards” (they rarely drop once they’ve risen), the failure to use reserves to hedge against these spikes ensures that the cost of living remains permanently elevated for the ordinary citizen.

Conclusion

The March 2026 MPC resolutions show a central bank that is “right” on the surface (interest rates and miner surrenders) but “silent” on the structural rot underneath. The lack of transparency regarding the ZiG’s exchange rate mechanism and the continued expansion of the money supply suggest that the currency’s stability is more fragile than the official reports indicate. For the market to regain confidence, the RBZ must move beyond terminology and address the practicalities of a multi-currency economy where the local unit is being forced into a corner.