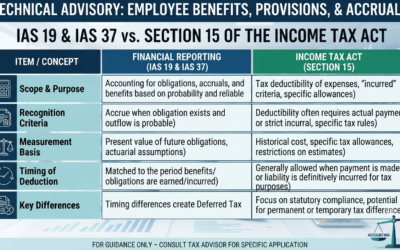

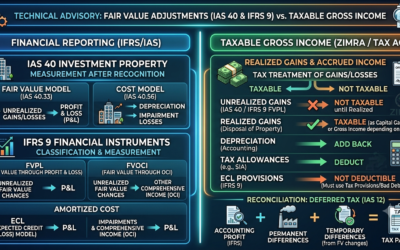

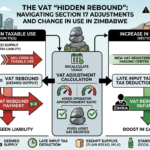

In the high-stakes world of Zimbabwean business, “Input Tax” is often seen as a one-time win-a deduction you claim when you buy a truck, a machine, or a laptop and then forget about. However, the Zimbabwean VAT Act [Chapter 23:12] contains a “sleeping giant” that most operators ignore at their peril: Section 17: Adjustments.

If you buy an asset for your business and later change how you use it or if the “mix” of your business changes-ZIMRA expects you to recalculate your VAT. This is the concept of VAT Adjustments and Change in Use. Failure to understand this is one of the most common reasons for massive “back-tax” bills during ZIMRA audits.

1. The Core Principle: Intention vs. Reality

When you register for VAT in Zimbabwe, the law allows you to claim back the VAT you paid on purchases (Input Tax), provided those purchases are used to make Taxable Supplies (sales that attract 15.5% or 0% VAT).

The problem arises when the reality of how you use an asset differs from your initial intention.

-

Scenario A: You bought a delivery van to deliver bread (Taxable), but now you use it primarily to move residential tenants’ furniture (Exempt).

-

Scenario B: You bought a building as an exempt residential dwelling, but you’ve now converted it into a commercial VAT-registered office.

In both cases, a Change in Use has occurred, triggering a mandatory VAT Adjustment.

2. Reduction in Taxable Use (The “Output Tax” Trap)

Under Section 17(2) of the VAT Act, if you previously claimed 100% Input Tax on an asset because you intended to use it for business, but you later start using it for “exempt” or “private” purposes, you have effectively “consumed” that VAT. ZIMRA views this as a Deemed Supply.

How the Calculation Works

You must pay back a portion of the VAT to ZIMRA. The formula generally used is:

Where:

-

A = The lesser of the Cost or the Open Market Value of the asset at the time of change.

-

B = The percentage of taxable use before the change.

-

C = The percentage of taxable use after the change.

The Example:

“Bhoora Logistics” bought a heavy truck for $100,000 (plus $15,500 VAT) in Jan 2026. They claimed the full $15,500 as Input Tax. By December, they decided to use the truck 40% of the time to transport “Exempt” goods (like unprocessed agricultural produce for a non-profit).

-

The truck is now worth $80,000.

-

The taxable use dropped from 100% to 60% (a 40% reduction).

-

Deemed Supply Value: $80,000 times 40% = $32,000.

-

VAT to Pay Back (Output Tax): 15.5/115.5 \times \$32,000 = $4,294.37.

If Bhoora Logistics doesn’t declare this on their VAT 7 return, they are essentially sitting on an undeclared tax debt.

3. Increase in Taxable Use (The “Hidden Refund”)

This is the side of the law businesses actually like, but often forget to claim. Under Section 17(5), if you bought an asset for an exempt purpose (and couldn’t claim VAT) but later started using it for your VAT-registered business, you can claim a Late Input Tax Deduction.

The Logic

ZIMRA allows you to “claw back” some of that VAT because the asset is now contributing to the fiscus through your taxable sales.

The Layman Example:

A doctor (exempt service) buys a high-end X-ray machine for $50,000 including VAT. Since medical services are exempt, she couldn’t claim the VAT back. A year later, she opens a “Commercial Imaging Center” that provides services to corporate insurance firms (Standard Rated).

-

She can now calculate the remaining “VAT value” in that machine and claim it as an adjustment on her next return, providing a massive boost to her cash flow.

4. The “Mixed Use” Nightmare: Apportionment

In Zimbabwe, many businesses are “Mixed Operators.” For example, a supermarket sells Taxable items (Coke, Soap) and Exempt items (Plain bread, Milk, Maize meal).

If that supermarket buys a new refrigerator, they cannot claim 100% of the VAT. They must apply an Apportionment Ratio based on their turnover.

-

The Overlooked Rule: If your ratio changes by more than 10% year-on-year, you are legally required to perform an Annual Adjustment on the last day of your financial year.

-

Most Zimbabwean accountants simply claim a fixed percentage all year and forget to do the “True-up” at year-end. During an audit, ZIMRA will do this math for you and they usually find that you owe them money.

5. Change in Use for Property Developers (Section 18D)

One of the most complex areas in 2026 involves residential property. Under recent amendments (including the spirit of Section 18D), if a developer builds a block of flats to sell (Standard Rated), they claim all the Input Tax on cement, bricks, and labor.

However, if the market is slow and they decide to rent out those flats instead of selling them, the use has changed from “Sale” (Taxable) to “Residential Lease” (Exempt).

-

The Consequence: The developer must suddenly “pay back” the VAT on the entire construction cost of those flats. For a multi-million dollar project, this “Change in Use” adjustment can bankrupt a developer overnight if they haven’t planned for it.

6. Why This is “Most Overlooked” in Zimbabwe

-

Complexity: The math A \times (B – C)) scares off many small business owners.

-

Tracking: Businesses don’t keep a “Fixed Asset VAT Register” that tracks the usage of an asset over time.

-

The “One-and-Done” Mentality: Many assume that once a VAT return is filed and accepted, that transaction is closed forever.

Conclusion: Audit-Proofing Your Business

In the era of TaRMS and real-time fiscalisation, ZIMRA’s algorithms are getting better at spotting inconsistencies. If your business sells both exempt and taxable goods, or if you frequently repurpose company assets for private use (like using the company “pool car” as a full-time family vehicle), you are likely sitting on an Adjustment Risk.

Summary Checklist for 2026:

-

Identify Capital Assets: Anything over $60 (excluding VAT) is subject to these rules.

-

Monitor Usage: If the taxable use of an asset drops by more than 10%, prepare for an Output Tax adjustment.

-

Annual True-up: Always perform an apportionment calculation at the end of your tax year.

-

Document Intent: Keep minutes or memos explaining why an asset’s use changed; it’s your only defense during an audit.