Preparing Your 2025 Income Tax Return: A Guide for Zimbabwean Businesses

As of early 2026, the deadline for the 2025 Income Tax Self-Assessment Return (ITF 12C) is looming on 30 April 2026. Under the new Tax and Revenue Management System (TaRMS), ZIMRA has streamlined the filing process, but the technical computations remain as rigorous as ever.

Having had four months since the 31 December 2024 year-end to finalize your financial statements, the focus now shifts from “accounting profit” to “taxable income.”

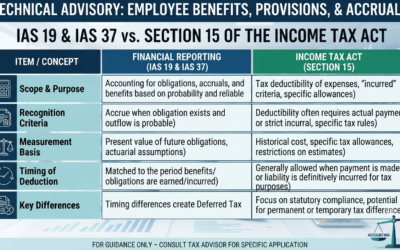

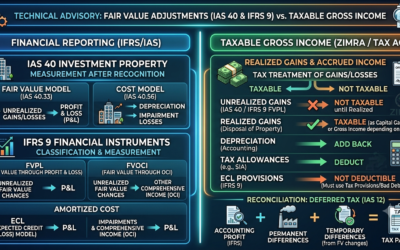

1. The Universal Computation Logic

Regardless of your VAT status, the starting point for any tax return is your Accounting Profit from the Income Statement. However, because accounting rules (IFRS) differ from the Income Tax Act [Chapter 23:06], you must adjust this figure:

2. VAT Registered vs. Non-VAT Registered Clients

The primary difference in computation lies in how you treat input costs and sales revenue.

A. Clients Registered for VAT

If you are a registered operator, your financial statements should generally be prepared net of VAT.

-

Income: Your gross income for tax purposes excludes the 15% VAT you collected (Output Tax), as that belongs to ZIMRA.

-

Expenses: You cannot claim the VAT portion of an expense as a deduction in your Income Tax return because you already “claimed it back” through your monthly/bi-monthly VAT returns (Input Tax).

-

Example: If you bought a laptop for $1,150 ($1,000 + $150 VAT), your deductible expense for income tax is only $1,000.

B. Clients NOT Registered for VAT

Businesses below the threshold (currently US$25,000) or those providing exempt supplies do not claim input tax.

-

Income: Your total collections are your gross income.

-

Expenses: You claim the full cost of goods and services, including the VAT paid to suppliers, as a deduction.

-

Example: Using the same laptop example, a non-VAT registered business would claim the full $1,150 as a base for capital allowances.

3. Dealing with Dormant Companies

A common mistake is assuming that “no trading” means “no filing.” If your company was dormant throughout 2025, you are still legally required to comply.

-

The “Nil” Return: You must log into the TaRMS portal and submit a Nil Return. This informs ZIMRA that there was no “accrual” or “receipt” of income.

-

Maintenance Expenses: If the company had fixed costs (e.g., secretarial fees, bank charges) despite not trading, these can be filed to create an Assessed Loss. This loss can be carried forward to offset future profits once the business resumes activity.

-

Status Update: If the dormancy is permanent, you should apply for the company to be placed on “Dormant Status” in the system to avoid future provisional tax estimates.

4. Crucial Reminders for the 2025 Tax Year

-

Currency Split: Under Section 37AA, you must report income in the currency it was earned. If you traded in both USD and ZiG (ZWG), your computation must reflect the 50/50 rule or the actual proportion, depending on your specific ZIMRA authorization.

-

Capital Allowances: Do not claim accounting depreciation. Instead, claim SIA (Special Initial Allowance) at 25% or Wear and Tear at the prescribed rates.

-

Aids Levy: Once you calculate your Income Tax (25%), remember to add the 3% Aids Levy on top of the tax amount.

Next Steps for Compliance

- Do you need assistance with doing your Income Tax return.

- Get in touch with us on 0771030251.