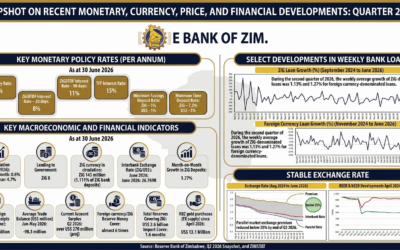

In January 2026, Zimbabwe reached an economic milestone that seemed impossible just two years ago: annual inflation dropped to 4.1%, the lowest level since the late 1990s.

Yet, for many businesses and consumers, the “celebration” feels expensive. The Reserve Bank of Zimbabwe (RBZ) has maintained a high-interest-rate environment, resisting calls for a “dovish” pivot (lowering rates) to stimulate growth. This disconnect raises a critical question: If prices are stable, why is the cost of borrowing still so high?

The answer lies in a hard truth of Zimbabwean macroeconomics: Low inflation does not mean low risk.

The High Price of Stability: Why Low Inflation Does Not Mean Low Risk in Zimbabwe

In the complex theatre of Zimbabwean macroeconomics, a curious paradox has emerged in early 2026. For the first time in years, the annual inflation rate has retreated to a disciplined single-digit figure. Under normal economic theory, this should signal a “pivot”—a moment for the central bank to slash interest rates, stimulate credit, and kickstart industrial growth.

Yet, the Reserve Bank of Zimbabwe (RBZ) remains hawkish. Interest rates remain stubbornly high, and the monetary “faucets” remain tightly shut.

This policy stance is not an oversight. It is a calculated admission that in Zimbabwe’s unique, quasi-dollarized environment, low inflation is a symptom of stability, not a guarantee of immunity.

The Achievement: Engineering a Low-Inflation Environment

The drop in inflation is a hard-won victory. It reflects a convergence of several reinforcing factors:

-

Tight Monetary Discipline: A “scorched earth” approach to liquidity management has successfully mopped up excess local currency.

-

The Gold-Backed Anchor: Improved foreign currency inflows—driven largely by the 2025–2026 gold bull market—have provided the ZiG with a tangible floor.

-

Subdued Domestic Demand: High interest rates have, by design, cooled consumer spending and cautious pricing behavior, preventing the “wage-price spiral” that haunted previous decades.

These are significant achievements. However, as the monetary authorities are keenly aware, they do not yet amount to structural immunity.

The Invisible Threat: Imported Inflation

The primary reason for the RBZ’s caution is that domestic policy cannot control external shocks. Unlike demand-driven inflation (caused by “too much money chasing too few goods”), imported inflation is mechanical and indifferent to local credit growth.

As the South African Rand (ZAR) strengthens against the US Dollar, the “landed cost” of South African goods—which comprise the bulk of Zimbabwe’s retail and industrial supply chain—rises automatically.

-

The Cushion Gap: In a fully sovereign economy, a strengthening trade partner’s currency can be offset by domestic exchange rate adjustments.

-

The Zimbabwean Reality: In a dollarized or quasi-dollarized economy, there is no “exchange-rate cushioning.” When the Rand gains power, the cost of imported fuel, electricity, and raw materials translates directly into higher shelf prices or decimated profit margins.

Interest Rates as an Insurance Policy

Maintaining high interest rates in a low-inflation environment is fundamentally an insurance play. The authorities are not fighting the inflation of today; they are insuring against the forward-looking shocks of tomorrow. If the RBZ were to ease policy prematurely, it would release a wave of liquidity at the exact moment that imported costs are rising due to the strong Rand. This “double whammy” could shatter the fragile confidence in the ZiG and re-anchor inflationary expectations upward.

High interest rates serve two defensive purposes:

-

Preventing Speculation: They ensure that it remains expensive to borrow local currency for the purpose of buying USD/ZAR on the parallel market.

-

Maintaining “Real” Value: They offer a high “real” return on holding local assets, incentivizing businesses to stay within the formal banking system despite external volatility.

The “Mirage” of Numerical Stability

Zimbabwe’s current single-digit inflation is a product of high-precision engineering. The introduction of the gold-backed ZiG in 2024, coupled with a ruthlessly tight monetary policy, has successfully mopped up excess liquidity.

However, this stability is not yet “structural.” It is “policy-induced.”

-

The “Lag” Factor: Inflation is a backward-looking metric. It tells us how much prices have changed. Interest rates, conversely, are forward-looking. They reflect the central bank’s confidence in the future.

-

The Ghost of Volatility: Because Zimbabwe has a history of rapid currency debasement, “inflation expectations” are sticky. If the RBZ lowers rates too early, it risks signaling that the “tight money” era is over, which could trigger a speculative rush back into the US Dollar, destroying the 4.1% achievement in a single quarter.

Why the Strong Rand Changes the Risk Equation

As discussed in our previous analysis, the South African Rand has strengthened significantly in 2026. This creates a specific type of risk that domestic interest rates cannot easily fix: Imported Inflation.

-

The Landed Cost Trap: Even if the domestic money supply is perfectly controlled, a strong Rand makes South African electricity, fuel, and raw materials more expensive in USD/ZiG terms.

-

The Buffer Requirement: Maintaining high interest rates acts as a “buffer.” It keeps the ZiG attractive to hold relative to other currencies. If the RBZ cut rates now, the ZiG would likely weaken against the Rand, making those vital imports even more expensive for the average Zimbabwean.

The “Structural Immunity” Problem

The authorities are waiting for “structural immunity”—a state where the economy can withstand a shock without collapsing the currency. We aren’t there yet for three reasons:

-

Critically Low Reserves: While gold reserves have grown, the “broad-money-to-GDP” ratio remains low. Zimbabwe does not yet have the deep foreign currency “war chest” needed to defend the currency if they stop using high interest rates as a primary defense.

-

The Shadow Economy: A large portion of Zimbabwe’s transactions still happen in the informal, USD-denominated sector. High interest rates in the formal banking sector are the only way the RBZ can exert influence over a system it only partially controls.

-

Forward-Looking Shocks: Geopolitical tensions or a sudden drop in global gold prices (which back the ZiG) remain “known unknowns.” High rates are the insurance premium the country pays to stay protected against these external events.

Conclusion: The “Insurance” Policy

For a Zimbabwean business owner, high interest rates are painful. They stifle expansion and make credit expensive. However, the alternative—a premature rate cut that leads to a currency crash—is terminal.

The monetary authority’s reluctance to ease policy is a sign of caution, not confusion. They are choosing to “over-insure” the economy’s stability rather than risk a return to the chaos of the early 2020s. Until the ZiG has been tested by a true external crisis and survived, “Low Inflation” will likely continue to sit alongside “High Interest Rates.”