The Finance Act No. 7 of 2025 and the 2026 National Budget represent a major overhaul of Zimbabwe’s tax system. The strategy shifts away from broad tax holidays toward a “compliance-first” model, focusing on digitizing the tax net and closing loopholes in capital-intensive sectors.

Below is a full analysis of the changes, the burden on taxpayers, and the resulting administrative complexity.

1. Mining & Energy Minerals

Mining faces the most aggressive changes as the state seeks to capture “windfall” profits from high commodity prices.

-

Taxes Added/Changed:

-

Tiered Gold Royalties: Replaced the 5% flat rate with a sliding scale: 3% if price $1,200/oz; 5% up to $2,499/oz; and 10% if price $2,500/oz.

-

Assessed Loss Restriction: Mines can now only carry forward 30% of their assessed losses to the next year.

-

Coal Levy: A new 2% levy on the gross value of coal (local and export).

-

Lithium/Chrome VAT: A 10% VAT on raw lithium and 5% on unbeneficiated chrome. Lithium sulphate (fully processed) is zero-rated ($0).

-

-

Burden: Very heavy on new projects; the loss carry-forward limit creates a “minimum tax” even if a mine is technically in the red.

-

Complexity: High. Requires complex valuation using international “Quoted Price Methods” to prevent transfer pricing.

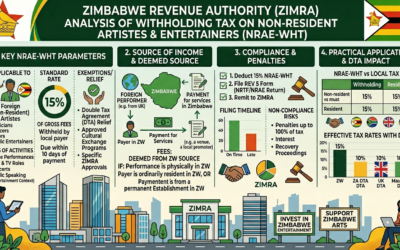

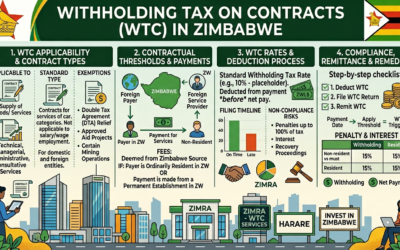

2. Banking & Financial Services

The sector is being leveraged as the primary enforcement arm for the revenue authority (ZIMRA).

-

Taxes Added/Reduced:

-

IMTT Reduction: ZiG-denominated Intermediated Money Transfer Tax fell from 2% to 1.5% and is now tax-deductible. The 2% rate remains for USD.

-

Digital Services WHT: Banks must withhold 15% on payments to foreign platforms (Netflix, Starlink, etc.).

-

-

Burden: Significant administrative cost for banks to implement real-time withholding.

-

Complexity: Critical. Systems must handle dual-currency tax logic and real-time data transmission via the TaRMS system.

3. Entertainment & Gaming

-

Taxes Added/Increased:

-

Bookmakers Tax: Increased to a final 20% on gross revenue.

-

Winnings Tax: Punters now face a 25% withholding tax on winnings.

-

Vatable Packages: Entertainment “bundles” that include exempt items are now treated as a single vatable supply at 15.5%.

-

-

Burden: Directly reduces the profitability of operators and the payouts for consumers.

-

Complexity: Medium. Simplifies corporate income tax but requires strict gross revenue tracking.

4. Real Estate & Construction

-

Taxes Added/Changed:

-

Special Capital Gains Tax (20%): Levied on the transfer of shares in entities that own land, closing the “company sale” loophole.

-

Rental Withholding Tax (10%): Landlords must withhold 10% from tenants who lack a tax clearance certificate.

-

Permanent Establishment (PE): For construction, a PE is deemed to exist from day one (previously 183 days).

-

-

Burden: High for foreign contractors and property developers.

-

Complexity: High. Landlords are now legally responsible for auditing their tenants’ tax status.

5. Manufacturing & Retail

-

Taxes Added/Reduced:

-

VAT Rate: Increased from 15% to 15.5%.

-

Going Concern VAT: Sales of businesses are no longer zero-rated (unless to government), adding a 15.5% cost to M&A deals.

-

Sugar Tax: Maintained at $0.001 per gram for beverages.

-

-

Burden: Inflationary; most costs are passed to consumers.

-

Complexity: Medium. Requires immediate software updates for all Fiscal Devices.

6. Agriculture & Tourism

-

Incentives & Levies:

-

Safari/Tourism: 2-year extension of duty suspension for tour operator vehicles.

-

Agriculture: New VAT exemptions for specific irrigation and rural electrification equipment.

-

-

Burden: Relatively light compared to other sectors, with a focus on recovery.

-

Complexity: Low. Standard administrative applications for duty waivers.

7. IT & Professional Services

-

Taxes Added:

-

Digital Services Tax: 15% withholding on all offshore digital services.

-

Professional Practicing Certificates: These will no longer be denied to employees if the employer is non-compliant, a rare relief for professionals.

-

BPO Incentives: Firms in Business Process Outsourcing get a 15% Corporate Tax rate and a $1,500 tax credit per youth employee.

-

-

Burden: High for local tech consumers; very low for export-oriented IT service firms.

-

Complexity: High. Defining “digital services” versus “software licenses” remains a technical challenge.

8. Transport & Logistics

-

Taxes Added/Changed:

-

Public Service Buses: Partial duty suspension (10% rate) for compliant operators; 0% duty for electric buses.

-

Operator Compliance: Haulage and bus operators must now maintain full books of accounts and register for Income Tax (ending presumptive-only models for large fleets).

-

-

Burden: Increases formalization costs for small fleet owners.

-

Complexity: Medium. Shift from flat presumptive taxes to profit-based assessment.

Summary Table: Tax Burden vs. Complexity

| Industry | Burden Level | Complexity | Primary Reason |

| Mining | Extreme | High | Loss carry-forward caps & tiered royalties. |

| Banking | Medium | Critical | Responsibility as the state’s withholding agent. |

| Real Estate | High | High | 20% tax on share transfers & 10% rental WHT. |

| IT/Tech | Medium | High | 15% Digital WHT and new BPO incentives. |

| Retail | Low-Medium | Medium | 15.5% VAT and mandatory fiscalisation. |