In Zimbabwe, the provision of entertainment—including hosting international artists, organizing concerts, and running events—is subject to Value Added Tax (VAT).

As of January 2026, the legislative landscape has shifted significantly following the 2026 National Budget and the Finance Act of 2025. Below is an article detailing the tax implications for the entertainment business.

Navigating the Spotlight: Tax Implications for the Entertainment Industry in Zimbabwe (2026)

The entertainment industry in Zimbabwe is no longer just about the “glitz and glamour”; it is now a highly scrutinized sector by the Zimbabwe Revenue Authority (ZIMRA). With the formalization of the economy, promoters and event organizers must navigate a complex web of taxes to remain compliant.

1. Value Added Tax (VAT): The 15.5% Standard

For any business providing entertainment, VAT is the most immediate consideration.

-

The New Rate: Effective January 1, 2026, the standard VAT rate in Zimbabwe increased from 15% to 15.5%.

-

Mandatory Registration: Under the Value Added Tax Act [Chapter 23:12], any business whose taxable turnover exceeds US$25,000 (or the ZiG equivalent) in a 12-month period must register for VAT.

-

The “Single Supply” Rule: A critical update in the Finance Act of 2025 addresses “mixed supplies.” If a promoter sells a ticket that includes entertainment plus “extras” like food or zero-rated programs, the entire package is now deemed a single taxable supply at the standard rate of 15.5%.

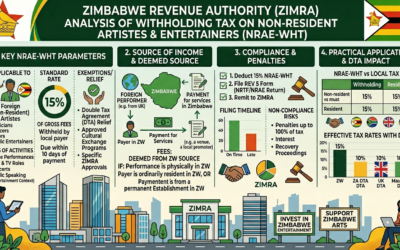

2. Hosting Foreign Artists: The “Imported Service” Trap

Bringing in international talent triggers specific tax obligations that often surprise promoters:

-

VAT on Imported Services: When a foreign artist provides a service (performance) to a Zimbabwean resident, it is considered an “imported service.” Under Section 21 of the VAT Act, the promoter is responsible for paying VAT on the value of the artist’s fee. As of 2026, this VAT must be paid in foreign currency.

-

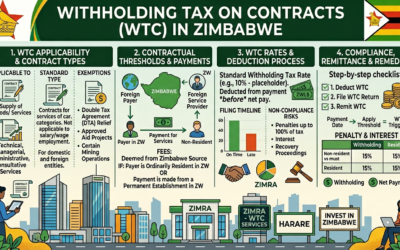

Non-Resident Tax on Fees (Withholding Tax): Promoters are legally required to withhold 15% of the gross fees payable to a non-resident artist. This must be remitted to ZIMRA within 15 days of the date of payment or when the fee becomes due.

3. Income Tax and Corporate Obligations

-

Corporate Income Tax (CIT): Entertainment companies are subject to a corporate tax rate of 25% on their net profits.

-

TaRMS Compliance: All tax filings must now be done through the Tax and Revenue Management System (TaRMS). To pay your taxes, you must have a valid Taxpayer Identification Number (TIN).

4. Digital Entertainment and Streaming

For businesses providing virtual gigs or digital content, the Digital Services Withholding Tax (DSWT) is now in force.

-

Legislation: Introduced in the 2026 Budget, this 15% tax targets payments made to foreign digital platforms (e.g., streaming services or international ticketing sites). Local banks act as agents, withholding the tax at the point of transaction.

5. Summary of Applicable Legislation

| Tax Type | Rate (2026) | Primary Legislation |

| Standard VAT | 15.5% | Value Added Tax Act |

| Withholding Tax (Artists) | 15% | Income Tax Act |

| Digital Services Tax | 15% | Finance Act of 2025 |

| Corporate Income Tax | 25% | Income Tax Act |

| IMTT (USD Transactions) | 2% | Finance Act (Various Amendments) |

Conclusion for Promoters

Providing entertainment in Zimbabwe requires meticulous tax planning. Failing to fiscalize ticket sales or failing to withhold tax on a foreign artist’s fee can lead to penalties that far exceed the profit of the event itself.